War Is Back — and It’s Driving Inflation

Why geopolitics, not central banks, now controls the price of everything

For much of the past three decades, inflation was treated as a technical problem. Central banks adjusted interest rates, governments managed fiscal balances, and global supply chains quietly delivered cheap goods across continents. When prices rose, the cause was assumed to lie somewhere within the economic system itself: excess demand, wage pressure, or monetary policy error.

That framework no longer explains the world we are living in.

Inflation today is increasingly shaped not by central banks but by geopolitics — by wars, sanctions, fractured supply chains, and the strategic weaponization of energy, trade, and technology. The return of great-power competition has quietly rewritten the rules of the global economy. And one consequence is becoming difficult to avoid: the price of everyday goods is now partially a function of geopolitical risk.

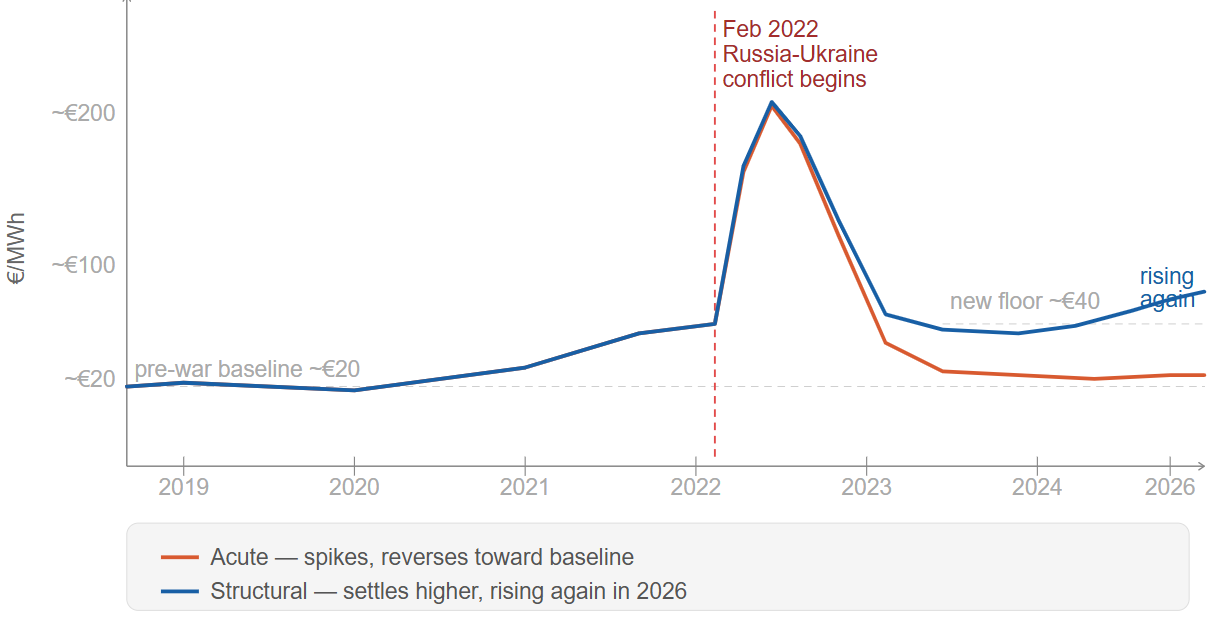

To understand why, it helps to distinguish between two types of geopolitical inflation. The first is acute: a conflict disrupts a supply route, energy prices spike, and markets adjust over months. The second is structural: the redesign of supply chains, the reorientation of trade policy, and the permanent addition of security considerations to decisions that were previously driven purely by cost. The first type can reverse. The second type compounds. Both are now operating simultaneously — and as of early 2026, the compounding is accelerating.

Inflation is no longer driven solely by cyclical economic forces. It increasingly reflects the cost of operating in a more contested world.

The era of cheap stability

The economic order that emerged after the Cold War rested on a powerful but largely unspoken assumption: geopolitics would remain dormant. Energy flowed predictably from Russia into Europe through pipelines. Manufacturing concentrated in China, where scale and low labour costs drove down global production prices. Maritime trade routes stayed open and secure, enabling supply chains to stretch across continents with remarkable efficiency.

Under these conditions, globalisation exerted a powerful disinflationary force. Between 1990 and 2020, global goods prices fell in real terms across most categories. The cost of clothing, electronics, and household goods dropped substantially as production shifted to lower-cost economies. Inflation did not disappear, but it became manageable — and economic policy, particularly monetary policy, was assumed to hold the decisive tools.

That assumption only held because the system operated within a broader environment of strategic stability. The peace dividend was not just a security phenomenon; it was an economic one. Cheap goods required cheap geopolitics. As that stability erodes, the economic model built upon it is beginning to unravel.

Energy: the first and most visible shock

Energy illustrates the transformation more clearly than any other sector — and with more precision than is usually acknowledged.

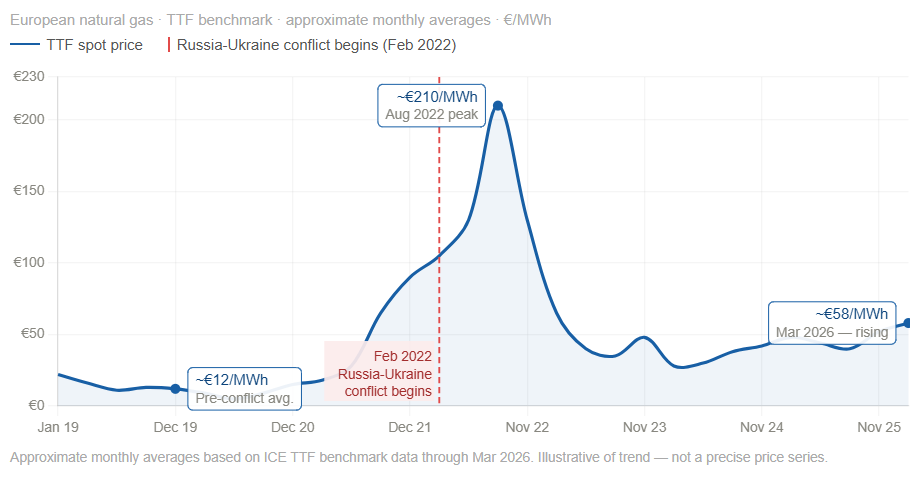

Before 2022, Europe relied on Russia for approximately 40 percent of its natural gas imports and roughly 27 percent of its oil. The arrangement was economically efficient, with Russian pipeline gas priced well below spot LNG rates for most of the 2010s. When the relationship collapsed following Russia’s full-scale invasion of Ukraine, Europe was forced to rebuild its energy architecture at extraordinary speed — and at extraordinary cost.

LNG imports to Europe roughly doubled between 2021 and 2023. Emergency regasification terminals appeared along coastlines from Germany to Italy. Germany alone spent over €200 billion on energy relief measures between 2022 and 2024 to shield households and industry from the price shock. Coal plants were temporarily reactivated. The European industrial base — particularly energy-intensive sectors such as chemicals, fertilisers, and aluminium — contracted sharply as input costs became uncompetitive.

These measures prevented immediate crisis. But they also revealed the structural cost of geopolitical rupture. Europe moved from dependence on a single pipeline supplier to dependence on global LNG markets, where prices reflect worldwide demand and geopolitical risk simultaneously. The system is more diversified — but it is also more exposed. A cold winter in Asia, a labour dispute in Australia, or a conflict near a key LNG terminal now transmits directly into European energy prices in ways that pipeline dependence never did.

By early 2026, European TTF gas prices — which had moderated from their 2022 peak of over €200/MWh to around €35-45 through much of 2024 and 2025 — have begun rising again. The proximate causes are familiar: renewed supply uncertainty, cold weather demand, and continued geopolitical friction along key shipping routes. But the underlying dynamic is structural. Europe did not return to its pre-war energy baseline. It settled onto a higher, more volatile floor — and that floor is now rising again.

Cheap goods required cheap geopolitics. The peace dividend was not just a security phenomenon — it was an economic one.

Supply chains: the slow structural shift

The supply chain story is less dramatic than the energy shock but ultimately more consequential, because it is structural rather than acute.

For decades, companies built supply chains around a single principle: cost efficiency. Manufacturing concentrated wherever labour was cheapest and logistics most streamlined. The canonical example is the semiconductor industry, which over forty years produced a global supply chain of extraordinary complexity and efficiency — with TSMC in Taiwan at its centre, producing over 90 percent of the world’s most advanced logic chips.

That concentration made economic sense for as long as Taiwan’s security was not in question. It no longer does. The CHIPS and Science Act in the United States committed $52 billion to domestic semiconductor manufacturing. The European Chips Act targeted €43 billion. Japan subsidised TSMC’s construction of a fabrication facility in Kumamoto. These are not marginal adjustments — they are the partial dismantling of a supply chain architecture built over four decades, driven entirely by geopolitical risk rather than economic logic.

The costs are direct and measurable. Building a leading-edge semiconductor fab in the United States costs approximately 30 to 50 percent more than building an equivalent facility in Taiwan, due to labour costs, regulatory requirements, and the absence of a mature supplier ecosystem. Those costs do not remain in the balance sheets of chipmakers. Over time, they appear in the prices of every product that contains a semiconductor — which is to say, nearly everything.

Critical minerals tell a similar story. China controls roughly 60 percent of global rare earth mining and a substantially larger share of processing capacity. Lithium, cobalt, and nickel — essential for electric vehicle batteries and grid storage — are concentrated in a small number of countries, several of which are politically unstable or increasingly aligned with adversarial powers. Western governments are now investing heavily in supply chain diversification, domestic processing capacity, and strategic reserves. Each layer of resilience adds cost that eventually reaches consumers.

Friend-shoring — the reorientation of supply chains toward politically aligned partners — is a rational strategic response. But it is also an inflationary one. The efficiency gains of the previous era were built on political indifference to origin. Reintroducing political criteria into sourcing decisions means accepting higher costs as a premium for security.

Shipping and chokepoints: compounding risk

A further source of structural pressure lies in the geography of global trade itself. Approximately 80 percent of global goods trade by volume moves by sea. Much of it transits through a small number of maritime chokepoints — the Strait of Hormuz, through which roughly 20 percent of global oil passes daily; the Suez Canal, which handles about 12 percent of global trade; the Bab el-Mandeb, which connects the Red Sea to the Gulf of Aden; and the Strait of Malacca, through which approximately 40 percent of global trade flows.

The Houthi attacks on Red Sea shipping beginning in late 2023 provided a concrete illustration of how quickly chokepoint disruption translates into economic pressure. Within weeks, major shipping companies rerouted vessels around the Cape of Good Hope, adding 10 to 14 days to transit times and roughly $1 million per voyage in additional fuel costs. Container freight rates on Asia-Europe routes increased by 150 to 200 percent at the peak of the disruption. Marine insurance premiums for Red Sea transit spiked to levels not seen since the height of Gulf tensions in the 1980s.

But the more consequential risk is not any single chokepoint in isolation. Europe’s post-2022 energy restructuring illustrates the paradox of geopolitical diversification. Replacing pipeline dependence with LNG imports looked like risk reduction on paper. In practice, it concentrated exposure along a small number of maritime corridors — Hormuz, Bab el-Mandeb, Suez — that are themselves now under simultaneous pressure. When chokepoints compound across the same supply chain, the nature of the shock changes: it stops being a sector-specific energy disruption and starts resembling a systemic logistics failure, with cascading effects across inflation, industrial output, and political stability.

This is no longer a hypothetical. As of early 2026, persistent disruption across multiple chokepoints is compressing the margins of the post-2022 energy architecture that Europe built at such cost. The question is no longer whether Europe is prepared for temporary crises — it demonstrably managed the 2022 shock. The question is whether it is prepared for persistent, simultaneous disruption across the supply chains it now depends upon. The answer, at this moment, is uncertain.

Central banks and the limits of monetary tools

This evolving landscape places central banks in a structurally difficult position — one that existing policy frameworks are not designed to address.

Monetary policy is effective against inflation driven by excess demand. Higher interest rates slow consumption, cool credit markets, and reduce the velocity of money through the economy. The textbook transmission mechanism works reasonably well when inflation originates in overheated domestic demand.

It works far less well against inflation rooted in geopolitical supply disruptions. Raising interest rates cannot reopen blocked shipping lanes. It cannot restore damaged energy infrastructure or rebuild a domestic semiconductor industry. Monetary tightening may suppress demand — and in doing so, may reduce the volume of goods exposed to higher costs — but it does not address the underlying structural drivers of price pressure. It manages the symptom while leaving the cause untouched.

This creates an uncomfortable policy dilemma. Tightening aggressively risks suppressing economic activity and investment at precisely the moment when industrial policy requires sustained capital expenditure on reshoring, supply chain diversification, and strategic reserves. Easing prematurely risks allowing structural inflation to become entrenched in expectations. Neither option is clean.

What this suggests is that price stability in the current environment requires tools that monetary policy cannot provide: industrial policy, alliance-based supply coordination, strategic energy reserves, and diplomatic frameworks that reduce the frequency and severity of geopolitical shocks. These are not primarily central bank instruments. They sit with governments, trade ministries, and foreign policy establishments — institutions that are only beginning to think in these terms.

What structural geopolitical inflation means in practice

None of this means inflation will remain permanently elevated at crisis levels. Acute shocks — energy disruptions, shipping crises — can and do partially resolve as markets adapt and alternative routes develop. The European energy shock of 2022 was severe; by 2024, European gas storage was at historically high levels and prices had moderated substantially from their peak.

But the structural layer does not resolve in the same way. Supply chains redesigned around security rather than efficiency do not revert to efficiency once the security concern passes — the investment has been made, the new architecture is in place, and the political constituency for maintaining it is now entrenched. Semiconductor fabs built in the United States and Europe will produce chips at above-market cost for as long as they operate. Strategic mineral reserves and diversified supply chains carry ongoing maintenance costs that pure efficiency systems do not.

The events of early 2026 — renewed energy price pressure, simultaneous chokepoint stress, and continued supply chain restructuring — are not aberrations from a stabilising trend. They are the structural condition asserting itself again. The baseline has shifted. The floor is higher and more volatile than it was before 2022, and the mechanisms that would return it to pre-war levels — a restoration of Russian energy flows, a resolution of maritime security threats, a reversal of supply chain nationalism — are not on any credible near-term horizon.

The practical implication is a higher baseline level of economic friction than the globalisation era produced — not a permanent inflation crisis, but a structural elevation in the cost of operating the global economy under conditions of sustained geopolitical competition. For investors, this means the three-decade disinflationary tailwind from globalisation has become a persistent headwind. For policymakers, price stability now requires engagement with strategic and foreign policy in ways the post-Cold War framework never anticipated. For ordinary consumers, a portion of the cost of living now reflects not supply and demand alone, but the distribution of power in the international system.

Conclusion

For a generation, economists assumed that globalisation had permanently subdued inflation. What they underestimated was how dependent that achievement was on a specific geopolitical condition: the absence of sustained great-power competition, the openness of global trade routes, and the willingness of major powers to prioritise economic efficiency over strategic security.

Those conditions are eroding — not gradually, but in compounding episodes that each reset the structural baseline upward. Wars disrupt energy flows. Strategic rivalry fragments supply chains. Maritime chokepoints become simultaneous pressure points. Each disruption introduces new costs into the global system — some acute and partially reversible, others structural and permanent.

Inflation, in this environment, becomes more than a macroeconomic indicator. It becomes a measurement of geopolitical instability — a signal embedded in prices that something in the underlying order of the world has changed. The fact that it is rising again in early 2026, three years after the initial shock, is not a surprise. It is the structure making itself visible.

Central banks can manage the demand side of this equation. They cannot manage the supply side, because the supply side is now partially determined by the conduct of states, the incidence of conflict, and the architecture of global power. That is a problem for which monetary policy has no answer — and for which the broader policy community is only beginning to develop the tools.

Follow on X: The Quiet Cartographer