The Squeeze: Venezuela, Iran, and the Stress-Testing of China's Energy Architecture

Ownership without access when chokepoints become instruments of pressure

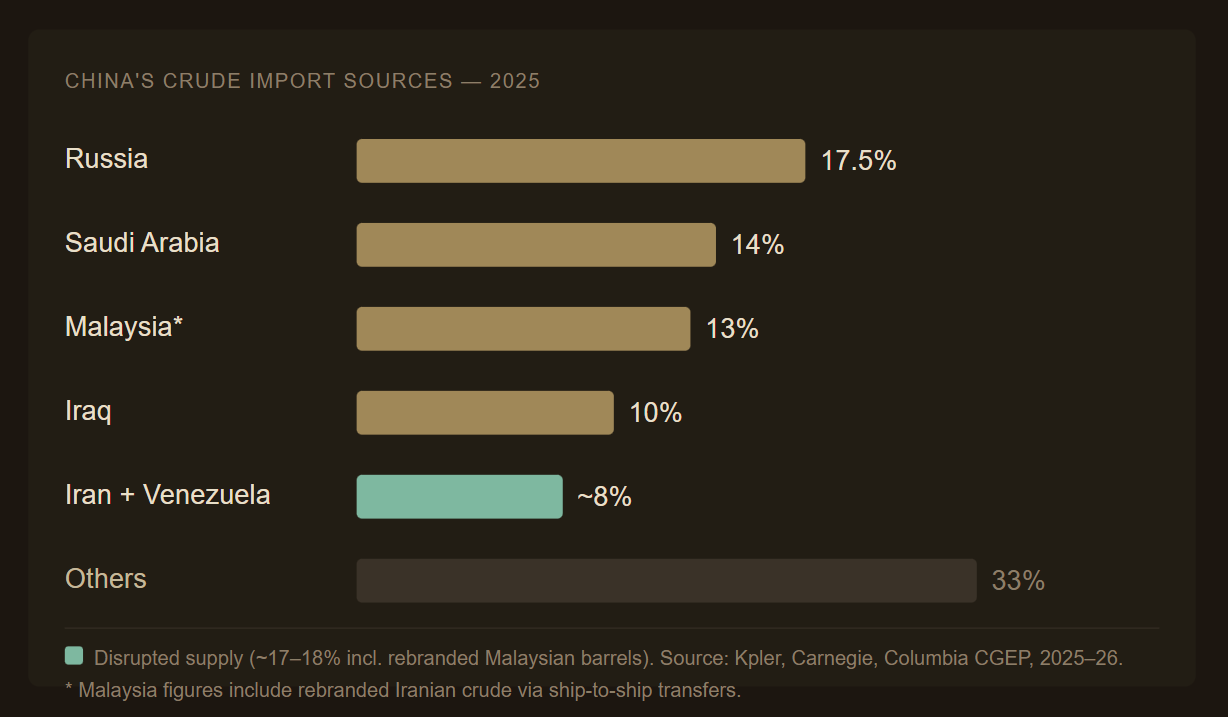

In the eight weeks between January 3rd and February 28th, 2026, China lost close to one-fifth of its total oil supply.

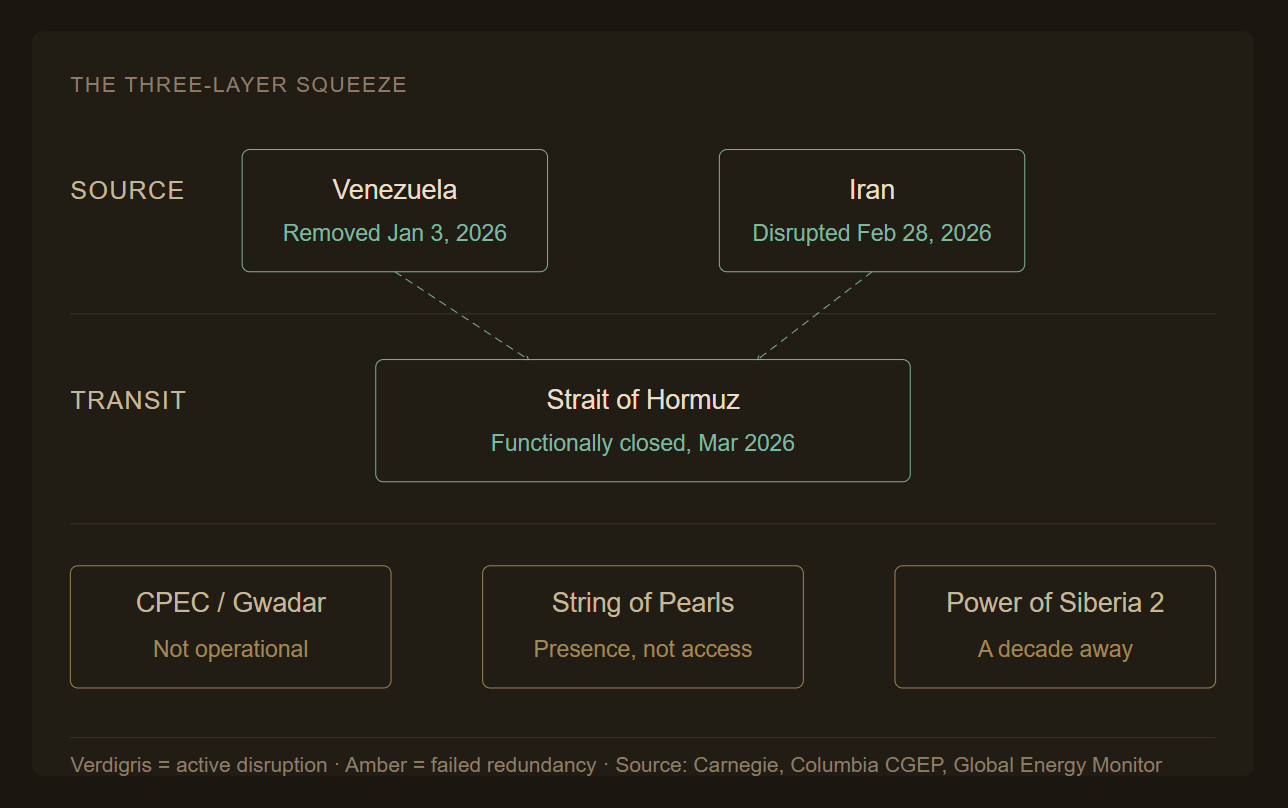

The first loss came from Venezuela. US special forces captured Nicolás Maduro and took operational control of the country’s oil sales, ending, at a stroke, China’s most reliable discounted heavy crude supply in the Western Hemisphere. Beijing had spent $106 billion building that position over two decades.

The second came from Iran. US and Israeli strikes triggered the effective closure of the Strait of Hormuz. Iranian crude, which alongside Venezuela had accounted for roughly 17 percent of China’s imports, was simultaneously disrupted.

Two theatres. Eight weeks. One-fifth of supply.

Whether this sequence reflects deliberate coordination or convergent strategic logic, its outcomes are consistent with a single objective: dismantling the energy architecture China has spent two decades building as an alternative to US-dominated maritime routes. The pattern is too precise, and the targets too well-chosen, to be read as coincidence. However, the more important question is not whether it was planned. It is why it worked, and why the architecture that was designed to prevent exactly this has proven more brittle than its architects anticipated?

The Architecture China Built

To understand what is being stress-tested, it helps to understand what was constructed.

China’s Malacca dilemma — the strategic vulnerability created by the fact that roughly 80 percent of its energy imports pass through the Strait of Malacca, a narrow waterway easily controlled by US naval assets, was formally identified in Chinese strategic planning in the early 2000s. The response was a multi-decade programme to build alternative supply routes that bypassed maritime chokepoints entirely, combined with a global port acquisition strategy that would give China physical presence across the Indian Ocean basin.

The String of Pearls — a network of Chinese-funded ports and facilities stretching from Hainan through the South China Sea, across the Indian Ocean, and into the Persian Gulf, was the maritime dimension. By 2025, China had its hand in more than 95 ports worldwide, with over 70 scattered across the Indian Ocean basin. Gwadar in Pakistan, Hambantota in Sri Lanka, Djibouti on the Horn of Africa, Kyaukphyu in Myanmar: each was a node in a network designed to project presence across the sea lanes that carry Chinese trade.

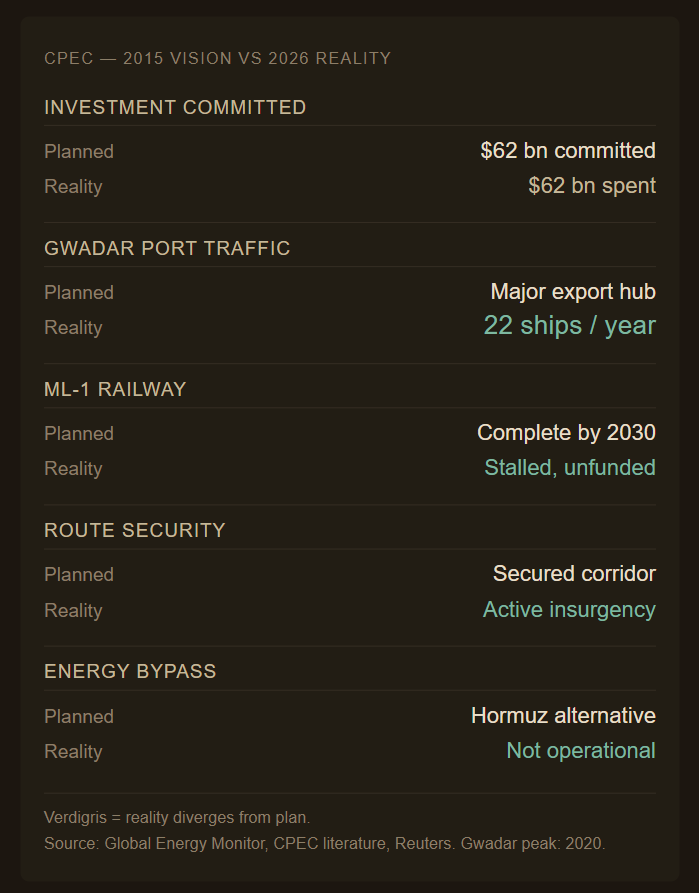

CPEC — the China-Pakistan Economic Corridor, was the overland complement. A $62 billion infrastructure investment connecting Xinjiang to the Arabian Sea port of Gwadar, it was conceived as a corridor that would allow Chinese energy imports to bypass Malacca entirely, arriving overland through Pakistan rather than through contested maritime straits. Beijing sold it as the gateway to a new continental trade architecture. Pakistani officials called it a game-changer.

The Power of Siberia pipeline system was the northern hedge, a direct energy supply from Russia that required no maritime transit at all, passing through no chokepoint that any external actor could close.

Together, these three initiatives with the northern hedge represented the most ambitious attempt by any state since the Cold War to build an energy security architecture independent of US-dominated maritime infrastructure.

What Has Happened to Each Pillar

CPEC and Gwadar: The Paper Gateway

The most striking failure of China’s alternative energy architecture is the one closest to its southern flank.

Gwadar was meant to be the Arabian Sea terminus that made the Malacca dilemma obsolete. The vision was straightforward: Chinese energy imports from the Gulf would arrive at Gwadar, travel overland through CPEC infrastructure, and reach western China without passing through a single contested maritime strait. On paper, it was an elegant solution.

In practice, Gwadar’s busiest year on record was 2020, when it handled 22 ships. The port that was meant to transform Pakistan into a logistics hub and China’s continental energy corridor sits largely idle. The reasons are structural, not accidental: insurgency in Balochistan has repeatedly targeted Chinese workers and CPEC infrastructure, making the overland route commercially uninsurable. The rail and road network connecting Gwadar to China remains incomplete. The energy transition infrastructure — pipelines, storage, distribution — was never built.

By early 2026, China had stepped back from Pakistan’s flagship ML-1 railway upgrade, the last major CPEC infrastructure project, after a Sharif government visit to Beijing failed to secure fresh funding. The corridor that was designed to make China’s energy imports land-route-secure has, after $62 billion in investment, produced a port that handles fewer ships per year than a regional Indian harbour.

The deeper principle CPEC illustrates is one that applies beyond this specific case: overland corridors are only as stable as the weakest political link in their transit chain. Infrastructure can be built across borders. The internal stability of the states those borders cross cannot be engineered from outside. China controlled the capital allocation. It could not control Balochistan.

The String of Pearls: Presence Without Access

China’s Indian Ocean port network exists and is operational. The strategic question is what it has actually purchased.

Ports provide commercial presence, not military access — at least not yet, and not reliably. Hambantota has become a politically toxic symbol of debt-trap diplomacy rather than a strategic asset. Djibouti hosts China’s only formal overseas military base but is geographically constrained and diplomatically complicated by the simultaneous presence of American, French, Japanese, and Italian military facilities. The Gwadar position, as described, is operationally irrelevant to energy transit.

More fundamentally, none of these positions solves the Malacca dilemma. The String of Pearls was designed to project presence, to give China the ability to protect its sea lanes. However, presence requires operational capability, rules of engagement, and allied relationships that China has not yet built at the scale the strategy requires. The ports are nodes in a network that doesn’t fully function yet, and the Hormuz closure has arrived before the network reached operational maturity.

The deeper irony: China’s port investments have given it real commercial leverage in the economies where those ports operate, but they have not given it the one thing the strategy was designed to produce — the ability to keep its own energy imports flowing when the maritime environment becomes hostile.

The Coherence of the Campaign

Taken individually, each event has a separate immediate cause. The Venezuela operation was framed as a law-enforcement action against a narco-state. The Iran strikes were framed as a response to nuclear and proxy threat. The Hormuz closure is Iran’s response, not Washington’s initiative.

However, the outcomes, read together, are consistent with a single strategic logic that has been visible in American policy planning for years: China’s critical vulnerability is energy import dependency through maritime chokepoints. If those chokepoints can be made unreliable — or if the supply sources that feed through them can be disrupted at origin — China’s economic model faces structural stress that its domestic buffers cannot indefinitely absorb.

The sequence has applied that pressure at three distinct layers simultaneously.

At the source layer, Venezuela and Iran — together accounting for roughly one-fifth of Chinese imports, have been disrupted or removed. These were not random targets. They were China’s primary discounted crude relationships: supply sources cultivated specifically to reduce dependence on US-aligned Gulf producers.

At the transit layer, the Hormuz closure has disrupted not just Iranian supply but the entire Gulf corridor through which China sources a substantial share of its remaining imports, including from Saudi Arabia, Iraq, and the UAE.

At the redundancy layer, CPEC’s failure means the overland alternative is unavailable at meaningful scale. The String of Pearls provides presence but not protection. And the northern hedge, which should have been China’s most reliable fallback, is where the pressure ultimately arrives.

What Has Not Been Dismantled

Precision requires acknowledging what the campaign has not achieved.

China’s domestic energy buffers are real. Strategic reserves are substantial, several months of supply at normal consumption levels. Teapot refiners in Shandong had accumulated approximately 1.4–1.5 million barrels per day of Iranian crude prior to the crisis. Renewables capacity — solar, wind, and nuclear — has been expanding aggressively and now covers a meaningful share of electricity generation, reducing oil dependency at the margin.

China is also not passive. Its position on the five-nation Hormuz safe passage list reflects the structural reality that Iran cannot afford to alienate its primary buyer. The safe passage was not diplomatically earned the way India’s was — it was economically inevitable. But it means Chinese supply chains are not as completely severed as the campaign’s architects might have intended.

What the three-layer pressure has achieved is not collapse. It is forced direction — pushing China toward the one supply relationship it has spent years trying to avoid making indispensable.

The Trap Within the Trap

Russia is the only actor that can provide large-scale, reliable, non-maritime energy supply to China in the short to medium term. That was true before the crisis. The crisis has made it urgent.

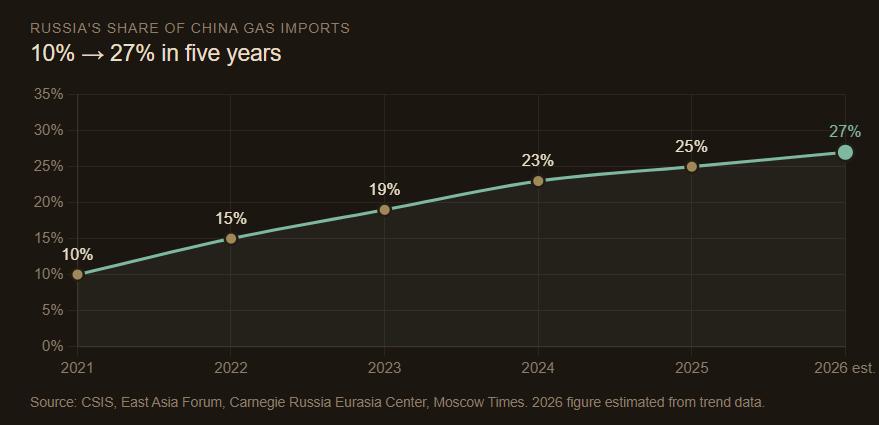

Power of Siberia 1 reached its planned capacity of 38 bcm this year. A “legally binding memorandum” on Power of Siberia 2 — which would add up to 50 billion cubic metres per year via Mongolia — was signed in September 2025. Russian gas, which accounted for 10 percent of China’s gas imports in 2021, had risen to over 25 percent by 2024. Russia is selling at prices 38 percent below its rates for other customers — approximately $248 per thousand cubic metres while other buyers pay $402.

On the surface, this looks like Chinese leverage: securing cheap supply from a sanctioned partner desperate for buyers. The deeper read is more uncomfortable.

Beijing’s informal policy has always been explicit: no single supplier should control too large a share of China’s energy market. For years, China applied that principle to Russia — deliberately stalling PoS2 negotiations, refusing to commit to price, volume, duration, or take-or-pay clauses. A project that could reach half capacity by 2034–2035 at the earliest was presented as a long-term option, not an urgent dependency.

The Hormuz crisis has rewritten that negotiation entirely.

With Venezuelan supply gone, Iranian supply disrupted, and Hormuz unreliable, China’s alternatives to Russian pipeline gas have narrowed to a degree that Moscow could not have engineered through diplomacy alone. Russia’s argument, that maritime routes can be cut off at any moment by Washington, so the only reliable option is pipelines from Russia, has just received its most powerful empirical confirmation in history. Every tanker that sat anchored outside the strait in March 2026 was an argument for Power of Siberia 2.

The pipeline China stalled for years to extract better pricing is now the infrastructure it needs urgently. And Russia’s negotiating position has never been stronger.

This is the trap within the trap. The squeeze was applied to China’s energy architecture. Its effect is to push China toward deeper dependency on the one supplier it was most carefully trying to avoid depending on, at the precise moment that supplier holds maximum leverage. What looked like a diversification strategy, accumulated over two decades and at enormous cost, has resolved under pressure into a managed dependency on Moscow.

Beijing built the architecture to avoid this outcome. The squeeze has made it almost inevitable.

What Comes Next

Three trajectories are now plausible, each following directly from the constraints the analysis has identified.

Accelerated Russian dependency. China moves faster on PoS2 than it intended, conceding on pricing and volume terms it previously refused. The overland supply relationship deepens, Russian leverage grows, and China’s informal one-supplier limit is quietly abandoned. This is the path of least resistance under current conditions — and the one Moscow is actively working to make inevitable.

Domestic acceleration. China treats the crisis as the forcing function its energy transition needed and sharply accelerates renewables deployment, nuclear capacity, and domestic gas production. This is already underway at the margin. The question is whether the political urgency generated by the crisis translates into the kind of institutional priority that moves timelines from decades to years. China has done this before — its solar manufacturing scale-up is the clearest precedent. The energy security version of that campaign is now more politically available than it was in January.

Relationship architecture — the India lesson. The five-nation safe passage list has demonstrated something Beijing has historically underinvested in: that relationships of genuine mutual dependency produce access that infrastructure alone cannot. China’s weight got it on the list. But weight requires continuous deployment and offers no surplus — no diplomatic goodwill, no post-crisis positioning advantage, no room in the negotiation that follows. If Beijing draws the right lesson from India’s Hormuz access, it begins building the relational architecture that its infrastructure strategy neglected. That is a generational project, not a crisis response. But the crisis has made its absence visible in a way that years of stable supply never did.

None of these trajectories is mutually exclusive. The most likely outcome is a combination of all three, sequenced by urgency: deeper Russian dependency now, domestic acceleration over the medium term, and a slow, uncomfortable reckoning with the limits of weight-based diplomacy over the long term.

The Closing Argument

The Malacca dilemma that animated two decades of Chinese strategic planning has not been solved. It has been joined by a Venezuelan dilemma, an Iranian dilemma, and a CPEC dilemma — each exposing a different assumption embedded in an architecture that was designed for a more stable world.

The deeper principle the crisis surfaces is this: under conditions of coordinated multi-layer pressure, the distinction between what you own and what you are permitted to use becomes decisive. China owns pipelines, ports, and corridors. What it discovered in the eight weeks between January 3rd and February 28th is that ownership and access are not the same thing — and that the gap between them widens precisely when the pressure is highest.

Infrastructure can be built. Access is granted. And in a world where chokepoints are weapons, the difference between those two things is the difference between an architecture and a strategy.

Beijing built the architecture. The squeeze has revealed what was missing.

Follow on X: The Quiet Cartographer

Some good insight, thank you. Once again illustrating why no one should underestimate the potential deliberacy of US action. And that as much as stress testing China, these actions also stress test NATO.