The Real Risk Isn’t Disruption. It’s Continuous Pressure.

Global trade is no longer breaking at single points. It is operating under sustained, multi-point pressure, and the system is struggling to adjust.

The most important shift in global trade over the past three years is not the one that made headlines. It is not the Houthi attacks on Red Sea shipping, or the elevated freight rates on Asia-Europe routes, or the rerouting of vessels around the Cape of Good Hope. These are symptoms. The underlying condition is structural: the global trade system has moved from episodic disruption to continuous pressure, and the mechanisms that previously allowed it to absorb and reset between shocks are no longer functioning as designed.

Europe’s post-2022 energy restructuring illustrates the dynamic precisely. What appeared on paper as diversification away from Russian pipeline dependence was, in practice, a shift toward a tightly coupled maritime system. Energy flows that were once regionally contained are now routed through a narrow set of global corridors — the Strait of Hormuz, Bab el-Mandeb, and the Suez Canal. These routes function less as passive transit channels and more as load-bearing structures within the global economy, carrying not only energy but the stability of interconnected supply systems.

The Strait of Hormuz alone handles approximately 20 to 21 million barrels of oil per day — close to one-fifth of global petroleum consumption, according to the U.S. Energy Information Administration. The same corridor carries roughly 20 percent of global LNG trade and a significant share of seaborne fertiliser flows, making it one of the most structurally critical nodes in the global trade architecture. When pressure accumulates at Hormuz simultaneously with instability at Bab el-Mandeb and friction in the Suez corridor, the system faces something qualitatively different from a single chokepoint disruption. It faces compounding stress across interdependent nodes — and that compound stress does not resolve the way isolated disruptions do.

The system has moved from episodic disruption to continuous pressure. The mechanisms that previously allowed it to reset between shocks are no longer functioning as designed.

From loose coupling to tight coupling

To understand why this matters, it helps to distinguish between two types of system architecture. A loosely coupled system retains flexibility because its components can absorb local shocks without cascading effects. A pipeline outage can be rerouted; a delay in one corridor can be offset through another. Disruption stays local because the system has slack.

The global maritime trade system, as it was configured before 2022, retained significant loose coupling. Energy flows moved through multiple routes with genuine redundancy. Supply chains maintained buffer inventory. Insurance markets priced individual route risk without assuming correlated shocks across corridors.

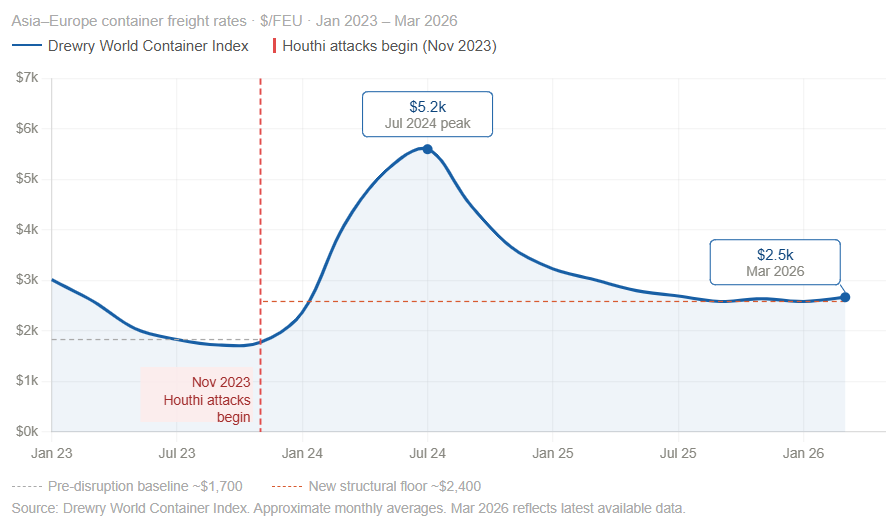

That architecture has been progressively tightened. Routing, pricing, insurance, and security now operate as interdependent layers: disruption in one forces adjustment across all others. When Houthi attacks made the Red Sea corridor unreliable, vessels rerouted to the Cape of Good Hope — adding 10 to 14 days to Asia-Europe transit and approximately $1 million per voyage in additional fuel costs. Insurance premiums for Red Sea transit spiked to levels not seen since the Gulf tensions of the 1980s. Container freight rates on Asia-Europe routes rose 150 to 200 percent at peak. Each of these adjustments was a rational individual response. Collectively, they represented the system repricing itself for a new baseline of risk — not a temporary spike, but a structural elevation.

The critical diagnostic is what happened next. Freight rates did not collapse as the immediate crisis phase passed. They adjusted upward and stabilised — the empirical signature of a system pricing in persistent risk rather than reacting to an isolated shock. A system that resets would show rates returning to pre-disruption levels as the immediate trigger fades. A system under continuous pressure shows exactly what the data shows: a new, elevated floor.

Freight rates didn’t collapse after the initial shock. They adjusted upward and stabilised — the empirical signature of a system pricing in persistent risk, not recovering from an isolated event.

When alternatives reproduce dependency

In principle, pressure at one point in a system should be relieved by shifting supply elsewhere. In practice, the alternatives available to the current system are more constrained than they appear.

Flows from Russia have become essential for major Asian importers, particularly India and China, which have absorbed discounted Russian energy at scale since 2022. But this is not a neutral substitution. It introduces exposure to sanctions risk, opaque logistics networks, and the pricing leverage of a single dominant supplier — reproducing in a different form the strategic dependency that Europe sought to escape. Similarly, Venezuelan supply remains contingent on U.S. policy decisions, limiting its reliability as a structural fallback. Gulf overland pipeline capacity exists but cannot substitute for maritime routes at the volumes required.

The deeper issue is that diversification has largely meant adding new nodes to the same underlying network rather than building genuinely independent pathways. When the network faces compound stress — simultaneous pressure across Hormuz, Bab el-Mandeb, and Suez — the new nodes are exposed to the same system-level disruption as the old ones. What appears as portfolio diversification is often, at the system level, a concentration of risk in the same set of maritime corridors.

Pressure doesn’t need to peak to matter

One of the less-discussed features of continuous pressure is that it shapes system behaviour even when it is not at its peak. The Red Sea provides the clearest current illustration. During periods of relative calm between Houthi attack cycles, the physical disruption is reduced — but the system adjustments made during active disruption do not fully reverse. Insurance premiums remain elevated. Vessel routing remains altered. Inventory strategies have shifted toward buffering against uncertainty rather than optimising for cost efficiency.

This is the mechanism through which continuous pressure differs from episodic disruption. A single acute shock, once resolved, allows the system to return toward its previous equilibrium. Persistent, credible threat — even at varying intensity — prevents that return. Companies, insurers, and logistics operators make durable decisions based on expected future risk, not just current conditions. Once a corridor is repriced as unreliable, that repricing tends to persist even through quieter periods, because the conditions that generated the risk have not structurally changed.

The practical consequence is that the cost of continuous pressure accumulates over time in ways that intermittent measurement misses. A freight rate spike that lasts three weeks and resolves is a manageable disruption. A freight rate that rises 30 percent and never fully returns to its previous level is a permanent increase in the baseline cost of global trade — one that feeds into manufacturing costs, consumer prices, and investment decisions across every sector that depends on maritime supply chains.

Beyond energy: the flow dependency problem

Energy disruptions attract attention because their price effects are immediate and highly visible. But the maritime corridors under pressure carry a much broader set of economic flows, and the interdependencies extend well beyond oil and gas.

According to UNCTAD, approximately 80 percent of global trade by volume moves by sea. The corridors linking Asia, the Middle East, and Europe carry not only energy but fertilisers, industrial inputs, consumer goods, and food. The fertiliser connection is particularly consequential: a significant share of global seaborne fertiliser trade transits Hormuz-linked routes, directly connecting energy corridor disruption to agricultural supply chains and food security in import-dependent regions.

Countries such as Saudi Arabia, Qatar, and the UAE — which control significant energy supply — are themselves heavily dependent on maritime imports for food, with India among their primary suppliers. When the same corridors that carry their energy exports also carry their food imports, the strategic calculus becomes genuinely complex: these states have both an interest in corridor security and an exposure to corridor disruption that creates incentives for stability even under geopolitical pressure.

What emerges from these interdependencies is not a set of discrete supply chains but a single flow system in which energy, food, industrial inputs, and consumer goods move through overlapping pathways. Disruption to any one flow category creates ripple effects across others — and when the disruption is systemic rather than localised, those ripple effects compound rather than cancel.

How the system absorbs pressure — unevenly

When stress builds across a tightly coupled system, its effects distribute unevenly according to each actor’s buffering capacity, strategic positioning, and exposure to the affected corridors.

China absorbs pressure through scale. Its strategic petroleum reserves, diversified import relationships, and domestic logistics capacity allow it to buffer shocks that would be more immediately damaging to smaller economies. But this buffering comes at a cost: maintaining strategic reserves, managing longer shipping routes, and accepting pricing premiums for supply security all reduce efficiency and increase the baseline cost of operating China’s import-dependent industrial system.

India navigates a more exposed position. Its rapid growth in energy consumption, combined with narrower reserve buffers and greater import dependence as a share of consumption, means corridor disruptions translate more directly into domestic price pressure. At the same time, India’s geography — and its strategic relationships with both Gulf suppliers and Western partners — gives it unusual flexibility to source from multiple directions, including discounted Russian supply. India operates within tighter margins but with more routing options than its reserve position alone would suggest.

Europe faces the most structurally uncomfortable position. Having made the transition from pipeline to maritime dependence at substantial cost, it is now exposed not just to price shocks but to sustained volatility — which is harder to manage than temporary scarcity. A price spike can be absorbed through emergency reserves and demand reduction. Persistent uncertainty about supply reliability requires structural changes to industrial planning, inventory management, and energy procurement that are far more expensive and slower to implement.

The corridor states — Saudi Arabia, Qatar, Türkiye, Egypt — occupy a different position again: they benefit from elevated energy revenues and strategic relevance, but they inherit the instability of the system they depend upon for transit. Türkiye’s control of the Bosphorus, Egypt’s management of the Suez Canal, and the Gulf states’ proximity to Hormuz give them leverage — but leverage in a system under stress is not the same as security.

The leading signal: insurance, not freight

If continuous pressure rather than episodic disruption is now the operating condition, the most diagnostic signal is not freight rates but marine insurance premiums. Freight rates are sensitive to current conditions and can spike rapidly in response to immediate disruptions — but they also recover when immediate conditions improve, which can create a misleading impression of normalisation.

Insurance premiums reflect something different: the market’s forward assessment of persistent risk. When underwriters price a corridor as structurally elevated rather than temporarily disrupted, it indicates a judgment that the conditions generating the risk are durable rather than transient. War risk insurance for Red Sea and Gulf of Aden transit, which spiked to 0.5 to 1 percent of vessel value per voyage during peak Houthi activity, had not returned to pre-2024 baseline levels as of early 2026 — even during periods of reduced attack frequency. That persistence is the market’s verdict on whether the disruption is episodic or structural.

Secondary signals worth tracking: inventory accumulation across supply chains (indicating that importers are buffering against uncertainty rather than running lean), repeated rerouting of vessels even during quieter periods (indicating that operators have updated their baseline risk assessment rather than temporarily adjusting), and naval deployment patterns in key corridors (indicating that states are treating the security environment as durable rather than temporary). Each of these, individually, is ambiguous. Together, and sustained over time, they constitute evidence of a system that has adapted to continuous pressure rather than one that is recovering from a shock.

Conclusion: a system that no longer resets

The question facing global trade in 2026 is not whether the system can withstand disruption — it demonstrably can, and has done so repeatedly over the past three years. The question is whether it can remain predictable, efficient, and broadly accessible when disruption becomes the operating environment rather than the exception.

The evidence suggests the answer is qualified at best. The system is adapting — rerouting, repricing, restructuring — but adaptation is not the same as resilience. A system that permanently reprices risk upward, that requires larger strategic reserves to maintain the same level of supply security, and that can no longer isolate disruption to individual corridors is a more expensive and less stable system than the one it replaced.

The structural conditions that produced continuous pressure — tightly coupled maritime routes, geopolitically contested corridors, limited genuine redundancy, and the concentration of critical flows through a small number of nodes — have not changed. If anything, they have become more entrenched as investment in the current architecture has deepened and alternatives remain constrained.

A system designed for stability under predictable conditions is now being asked to function under continuous, distributed strain. It is doing so — but at a cost that is accumulating quietly in freight premiums, inventory buffers, supply chain restructuring, and industrial planning adjustments across the global economy. The disruption is not visible in a single dramatic event. It is visible in the baseline.

Follow on X: The Quiet Cartographer

Additional interesting sources worth exploring:

Great read! The way you laid out disruption as an event to disruption as an operating condition makes sense. What's alarming is how the system keeps looking alright on the surface while the margins for absorbing the next shock keep disappearing beneath the surface. Do you think that gap between visible stability and invisible fragility ever closes on its own, or does it just widen if something forces a redesign? Thanks for the write-up!