The Geometry of Crisis

The crisis that priced the difference between alliance and access

In late March 2026, Iranian Foreign Minister Abbas Araghchi confirmed in public statements that five countries — China, Russia, India, Iraq, and Pakistan — would be permitted to transit the Strait of Hormuz. The precise formulation varied across sources; what was consistent was the category: friendly nations, defined not by formal alliance but by the relationships Tehran had built and chosen to honour under maximum pressure.

Five names. Not five allies. Five relationships, each earned on different terms, over different timescales, through entirely different logic. That list, more than any price chart or diplomatic communiqué, is the most precise summary of the new geopolitical order to emerge from the Hormuz crisis. It tells you, in the starkest possible terms, which foreign policy architectures produced access when it mattered most — and which did not.

The question worth asking is not who lost. It is what the crisis made legible about who was already positioned. The world has quietly sorted itself into three tiers: the sanctioned, the scrambling, and those who were, in a word, positioned. Understanding what placed each name on that list explains more about the next decade of geopolitics than most strategy documents will.

Russia: The Accidental Architect

Russia did not plan to benefit from the Hormuz closure. It simply built, over the four years since its invasion of Ukraine — the supply infrastructure, the shadow fleet, and the bilateral energy relationships that made it indispensable the moment Gulf supply collapsed.

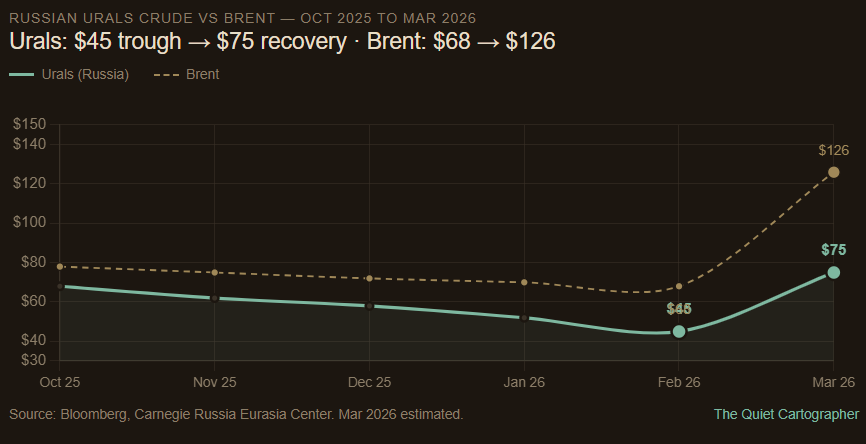

The numbers are striking. Russian Urals crude, which had been trading at approximately $45 per barrel in February 2026, jumped to around $75 in March as Asian buyers scrambled for alternatives to stranded Gulf barrels. At that price differential, the Russian budget was receiving roughly $1.63 billion in additional monthly tax revenue for every $10 increase in crude price. The Kremlin’s oil revenues, which had fallen nearly 50 percent year-on-year in the first two months of 2026, recovered to their highest level since the 2022 invasion of Ukraine. In some cases, Russian crude was selling in India at a premium to Brent — a complete reversal of the sanctions-era discounts that had defined Russian exports for four years.

The broader context makes this more significant. Before the crisis, Russia was drawing down its National Wealth Fund to cover military expenditures that had grown by 5.8 percent in early 2026. The Hormuz crisis arrived as a fiscal lifeline at the precise moment the Kremlin needed it most.

What Russia has secured exists on two different timescales, and conflating them overstates the case. The price windfall is cyclical — it will compress as alternative supply comes online, as strategic reserves are released, and as the crisis eventually de-escalates. Russia will not sustain $75 Urals indefinitely. That gain is real but temporary.

What is structural is different: the emergency US waiver allowing buyers to purchase Russian crude without triggering sanctions — initially granted to prevent a total fuel collapse and then extended — has effectively rehabilitated Russian oil in global markets with Washington’s implicit endorsement. The policy logic of maximum pressure on Iran destroyed the policy logic of maximum pressure on Russia. The two objectives were incompatible, and energy security won. The buyer relationships re-established under that waiver — India deepening its Russian crude dependency, Asian refiners rebuilding logistics chains around Russian supply — will not simply evaporate when the waiver expires or when Brent falls back below $100.

Russia is not the biggest winner of the Hormuz crisis. But the structural dimension of its gains — legitimacy, not price — may prove the most durable.

India: The Proof of Concept

India’s position on the five-nation list is the most analytically interesting, and the most misread in Western commentary.

Consider the sequence. On 25 February 2026, three days before the strikes on Iran, Prime Minister Modi arrived in Tel Aviv for a state visit. He addressed the Knesset — the first Indian leader to do so — and declared: “India stands with Israel firmly, with full conviction, in this moment and beyond.” The two countries elevated their relationship to a Special Strategic Partnership, signing 27 bilateral outcomes including joint development of defence platforms, an Indo-Israel Cyber Centre of Excellence, and the India-Israel Innovation Centre for Agriculture. India is, by any measure, Israel’s largest weapons buyer.

Twenty-eight days later, Iran granted India’s vessels safe passage through a strait it had closed to every US ally and every Gulf state supporting the conflict.

India maintained both relationships simultaneously, under maximum pressure, without flinching from either. This is not a tightrope. It is the strategy itself, demonstrated under conditions that tested it as severely as possible.

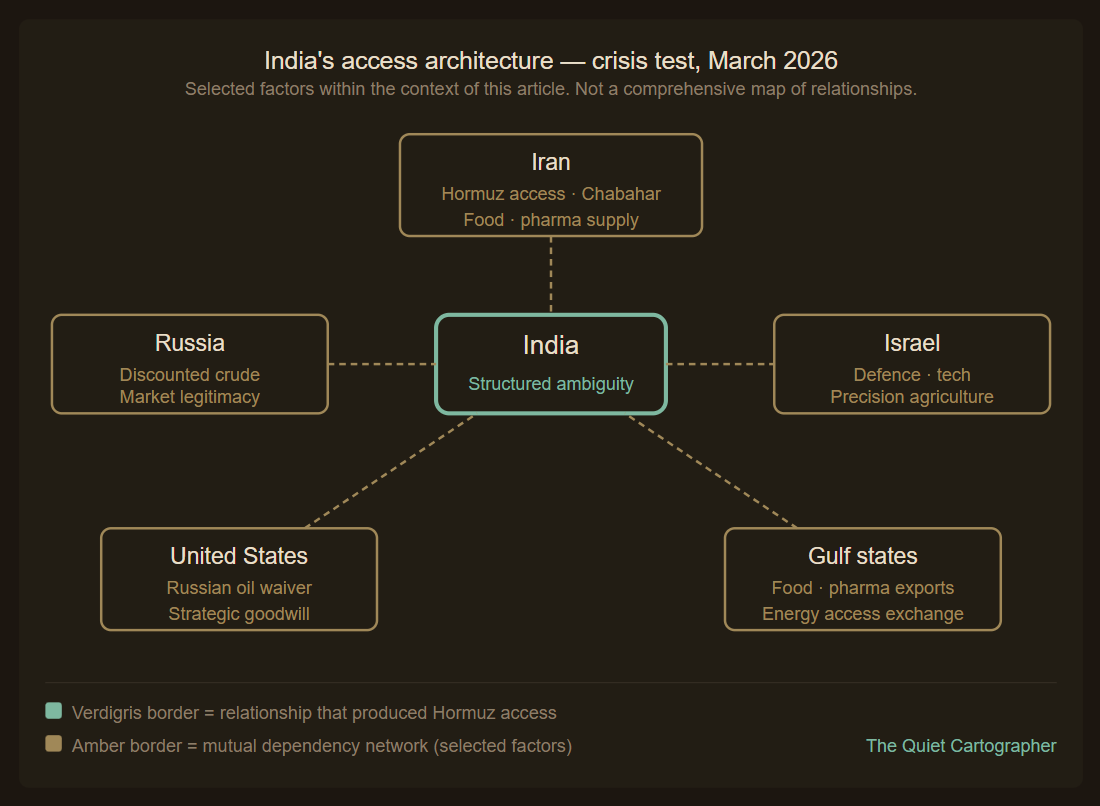

What India has built, over the past decade, is what its diplomats call strategic autonomy but what is more precisely described as structured ambiguity — the deliberate maintenance of relationships that, from any single actor’s perspective, appear contradictory, but that from New Delhi’s perspective form a coherent access architecture. The Hormuz crisis is the first major stress test of whether that architecture holds. It held.

Map the geometry. With Iran, the relationship runs deeper than most Western observers credit. India imports roughly 40 percent of its crude oil and over 54 percent of its LNG through Hormuz-adjacent routes, making the Gulf the single most consequential supply corridor for the Indian economy. Beyond energy, Iran’s recognition of India as a “friendly nation” reflects years of careful cultivation — the Chabahar port agreement, the non-participation in Western sanction coalitions, and a consistent pattern of direct diplomatic engagement rather than multilateral pressure. When the crisis came, India’s LPG carriers — the Pine Gas, the Jag Vasant, the BW Tyr, the BW Elm — received IRGC clearance and transited the strait. The diplomacy had been done years before it was needed.

What structured ambiguity secured was access, not immunity. India’s Hormuz dependency — 40 percent of crude, 54 percent of LNG — remains structurally unchanged. The crisis demonstrated that India’s relationships could keep those routes open under pressure. It did not demonstrate that India could function without them. The architecture reduced the risk; it did not eliminate the exposure. That distinction matters for what India’s success here actually proves.

With Russia, the relationship is equally deliberate. When the US Treasury issued a 30-day waiver allowing buyers to purchase stranded Russian oil, India was a primary beneficiary — and notably received its waiver before broader G7 markets. India gets supply security; Russia gets price recovery and a market that legitimises its exports at a moment of international isolation. It is a mutual arrangement constructed on the back of four years of discounted crude purchases that the West repeatedly pressured India to abandon.

With the United States, the relationship is managed rather than maximised. India acknowledged the Russian oil waiver, deflected pressure to formally align against Iran, and maintained its position as a recipient of American goodwill without ever becoming a full instrument of American strategy. When Washington needed India to absorb Russian crude to prevent a broader market collapse, India was positioned to do so — and extracted the waiver as the price of that service.

What India is exchanging for this access is material and consequential. The Gulf Cooperation Council states — which import 80 to 90 percent of their food through maritime trade — are among the primary buyers of Indian agricultural exports. Rice, wheat, pulses, basmati: the Middle East represents roughly 70 percent of demand for Indian basmati rice alone. As the Hormuz closure strangled Gulf food imports, India’s Hormuz access made it the only major Asian agricultural exporter capable of reliably supplying these markets. Food security and energy access have become the terms of the same negotiation — conducted through years of relationship rather than crisis-period haggling.

The pharmaceutical dimension adds another layer that has gone largely unnoticed. The Persian Gulf is not just an energy chokepoint. It is a critical pharmaceutical transit corridor, with roughly 80 percent of the region’s $23.7 billion pharmaceutical trade depending on medicines or their ingredients passing through — the vast majority of which originate in India. With air cargo capacity in the Gulf region down 79 percent and shipping at 90 percent below pre-war levels, India’s pharmaceutical industry is the primary source of supply continuity for a region that cannot otherwise function. On 28 March 2026, India sent 38,000 metric tonnes of fuel to Sri Lanka after its regular Gulf suppliers invoked force majeure. Similar requests arrived from Bangladesh, Nepal, and the Maldives. India had secured its own access from Iran, and was deploying it regionally within days.

The India-Israel relationship, far from being a complication, is the clearest demonstration of why the architecture holds. Israel is India’s second-largest defence supplier after Russia. The Special Strategic Partnership formalises cooperation in AI, quantum computing, cybersecurity, precision agriculture, and joint weapons development. These are not concessions to Western alignment — they are national capability investments that India pursues regardless of their geopolitical optics. Deepening this partnership three days before a war that Iran is fighting, and receiving Iranian safe passage twenty-eight days later, is not despite the contradiction. It is the mechanism.

India did not get on the five-nation list because of neutrality. Nor, more precisely, did it get there through strategy alone. What placed India on the list is that multiple actors needed it simultaneously — Iran needed a market and a friendly face; Russia needed legitimacy; the Gulf states needed food and medicine; Washington needed India to absorb Russian crude without triggering a broader market collapse. India’s structured ambiguity worked not merely because New Delhi built the right relationships, but because it built them with actors whose needs, at the moment of maximum pressure, converged on India as the indispensable partner. Strategy created the position. Mutual dependency activated it. Both matter — and overstating the role of intent at the expense of the second risks turning analysis into attribution.

China: The Weight of Structural Position

China was always going to be on the list. That is both its strength and its strategic limitation.

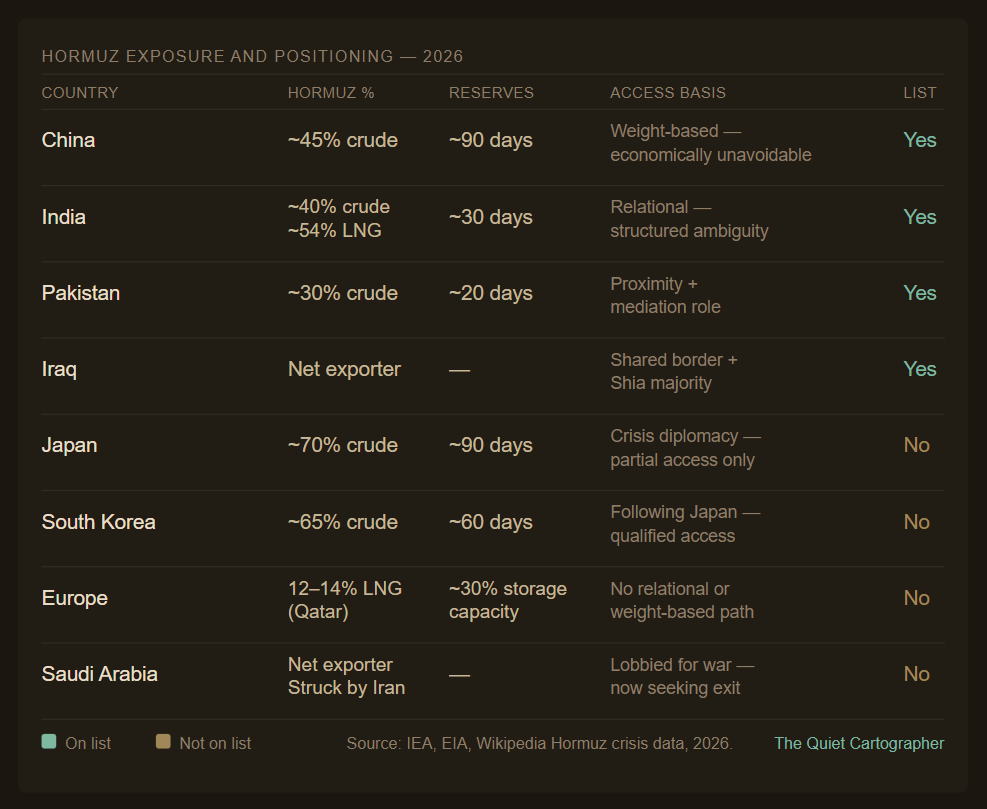

Iran cannot afford to alienate China. It is not a close call. China purchases more than 80 percent of Iran’s exported oil — the only major buyer willing to absorb Iranian crude at scale despite Western sanctions. China has invested over $100 billion in Iranian energy and infrastructure projects. The safe passage was structurally inevitable, not diplomatically earned in the way India’s was.

China’s Hormuz access tells us less about its diplomatic architecture and more about the weight it carries by virtue of scale. That weight is real and substantial. Beijing holds approximately a billion barrels in strategic oil reserves — several months of supply — accumulated during the period of global oversupply. Its domestic refining overcapacity and the stockpiling behaviour of independent teapot refiners in Shandong created additional buffers. Where Japan and South Korea faced immediate acute pressure, China absorbed the shock — more expensively than usual, but without system failure.

China’s position carries a constraint that India’s does not. Beijing declared itself a neutral country — unwilling to alienate whatever post-war regime might emerge in Iran, and careful not to compromise its $100 billion in infrastructure investments. That neutrality is a choice with costs. China is not positioned as a mediator, a trusted partner, or a constructive actor. It is positioned as a silent beneficiary — present in every relationship that matters, dominant in none, and formally committed to nothing.

India builds access through relationships of genuine mutual dependency. China builds access through economic weight and infrastructure investment. Both produced safe passage. When Iran needs reconstruction financing, when Gulf states need to rebalance dependencies, when the post-crisis diplomatic architecture is being negotiated, India will be politically present in ways China will not. China will remain economically unavoidable — its financing, its demand, and its long-term infrastructure commitments will shape outcomes whether or not Beijing is at the table. Visible political agency on one side; structural economic gravity on the other. Both are forms of power. They produce different kinds of influence — and different constraints.

Pakistan: The High-Wire Act

The one idea that organises everything Pakistan is doing in this crisis is this: it is a state that has learned to leverage its position between systems — between the US and China, between Sunni and Shia, between mediator and arms conduit — simultaneously and without formal commitment to any of them. That positioning is Pakistan’s primary strategic asset, and the crisis has forced it into its most demanding deployment yet.

The evidence is dense. Pakistan emerged as host and convener of the STEP grouping — Saudi Arabia, Turkey, Egypt, and Pakistan — the most coordinated regional diplomatic initiative attempted since the war began. Field Marshal of the Pakistan Army, Asim Munir served as the key interlocutor delivering a US 15-point proposal directly to Iran. In return, Iran granted 20 Pakistani-flagged ships transit at two per day. The talks hit a major roadblock on 30 March — no concrete roadmap, no resolution of the core sticking points. A senior Pakistani source captured the condition precisely: “We can take the horse to the water; whether the horse drinks or not is entirely up to them.” Diplomatic centrality without closing leverage.

The constraints arrived simultaneously. A bomb exploded near Pakistan’s embassy in Tehran on 29 March. Pakistan’s defence establishment issued a direct public warning to Israel — calibrated carefully enough to protect the Iran relationship without destroying the mediator role Washington is relying on. Every move serves multiple audiences at once. None of them can be fully satisfied. This is the same architecture India operates, compressed into a narrower margin and under acute, immediate pressure.

The deeper structural story — the one that has received almost no analytical attention — is the China-Pakistan-Saudi defence technology pathway. The Saudi-Pakistan Strategic Mutual Defence Agreement, signed in September 2025, created an opening for Chinese military technology to enter the Gulf’s security architecture without China needing to be formally present. Saudi Arabia, historically anchored entirely within the US defence procurement system, is now in a relationship with Pakistan whose military ecosystem runs on Chinese technology. Beijing does not need to sign an agreement with Riyadh. It needs Pakistan to deepen what it has already built.

Alongside this, Pakistan has offered the US development rights to a naval base at Pasni on the Arabian Sea — explicitly framed as a counterbalance to Gwadar and an expansion of US strategic reach near Iran. The same sovereign access asset, offered to China and the United States simultaneously, in adjacent ports on the same coastline. A state with one primary tradeable resource, deploying it bilaterally with every actor that holds leverage, in the hope that the combination produces the security that neither relationship alone can guarantee.

Whether it will work is genuinely uncertain. What is not uncertain is the ambition — or the risk if it doesn’t.

The Ones Not On The List

The five-nation list is most clearly understood by examining who is absent — and what they are doing about it.

Japan sources approximately 95 percent of its crude from the Middle East, with around 70 percent arriving through Hormuz. South Korea faces an equivalent structural exposure. Neither is on the list. Both are now attempting, in real time, what India built over a decade: Araghchi confirmed Iran is prepared to allow Japanese-related vessels to transit after official consultations, with South Korea’s foreign minister stating Seoul would follow Japan’s lead. Crisis-period diplomacy is producing partial, qualified access — Iranian goodwill extended as a confidence measure, not as a durable architectural commitment. The question these negotiations pose is precise: can you build in weeks what India built in years? The evidence so far suggests partial access at best, not structural positioning.

Europe receives 12 to 14 percent of its LNG from Qatar through the strait. Dutch TTF gas benchmarks nearly doubled to over €60/MWh by mid-March, arriving on top of historically low storage levels following a harsh winter. The European Central Bank postponed planned rate reductions and raised its 2026 inflation forecast. European industry faces surcharges of up to 30 percent from chemical and steel manufacturers. Europe is not on the list, and has no obvious path to it — it has neither the energy relationship with Iran that India cultivated, nor the economic weight China deploys, nor the geographic and cultural proximity Pakistan is leveraging.

Saudi Arabia’s absence deserves its own paragraph, because Saudi Arabia lobbied for this war and is now one of its most exposed casualties. Crown Prince Mohammed bin Salman pressed Washington repeatedly to strike Iran. The strikes came. Iran hit Riyadh and the Eastern Province. Saudi Arabia now finds itself running backchannels to Tehran to contain a conflict it helped ignite, while Trump presses Riyadh to join the Abraham Accords as the price of continued security guarantees. The relationship assumed to be the bedrock of Gulf security — unconditional US protection in exchange for oil supply and dollar recycling — is now transactional in both directions. Neither side is entirely comfortable with what the transaction has become.

Every unlisted state failed for the same reason, and it is worth naming plainly. Japan, South Korea, Europe, and Saudi Arabia did not fail to get on the list because of bad luck or insufficient leverage. They failed because they had built their security architectures around systems — alliances, institutional guarantees, market mechanisms, formal multilateral frameworks — rather than around the bilateral, diversified, deliberately ambiguous relationships that produced access when those systems stopped functioning. The five-nation list is not a ranking of military power or economic size. It is a ranking of relationship architecture. The states that relied on the architecture of the last eight decades discovered, in the space of eight weeks, that it was not designed for this kind of pressure.

The US-led alliance system provided no energy access advantage during this crisis. Alliance membership was, if anything, the disqualifying criterion for Hormuz access. The security guarantee and the supply guarantee pointed in opposite directions — and when forced to choose, states discovered that the guarantee they had paid for did not cover the risk they actually faced.

The Closing Argument

The Hormuz crisis has run a live experiment on which foreign policy architectures produce energy access under maximum stress. The results are in. The five-nation list is the data.

Privileged access has become a geopolitical asset class — as real as territory, as durable as treaty alliances, and more flexible than either. It cannot be purchased in a crisis. It can only be accumulated over years of relationship investment that, during normal times, appears diplomatically untidy, strategically ambiguous, and analytically uncomfortable.

Russia benefited from a windfall it did not plan, with gains that are partly cyclical and partly structural — and the structural part will outlast the price. China was protected by weight it spent decades accumulating, and will shape outcomes through economic gravity whether or not it achieves political visibility. India was positioned by relationships it spent decades cultivating, activated at the moment of maximum pressure by the convergence of multiple actors’ needs on a single indispensable partner. Pakistan is attempting, under acute pressure and with certain skill, to build a version of the same architecture in real time — with less margin, more risk, and an outcome that remains genuinely open.

Beneath these individual positions, a structural transition is underway that the list only partially captures. China is acquiring influence in the Gulf’s security architecture through Pakistan’s defence ecosystem — without formal presence, without signed agreements, without a single public commitment. Saudi Arabia, the anchor of the old order, is hedging simultaneously toward Washington and Beijing, running backchannels to Tehran while accepting Chinese-system technology through its Pakistani defence partner. The US-led architecture that structured Gulf security for eight decades is not collapsing — but it is no longer the only architecture operating in the region. A second one is assembling quietly, indirectly, and without announcement.

The uncomfortable implication — the one this piece cannot resolve — is for the states that cannot build what India built. Structured ambiguity at India’s scale requires diplomatic bandwidth, economic weight, domestic political tolerance for apparent contradiction, and a decade of patient relationship cultivation with actors that most Western-aligned states are institutionally and politically prevented from engaging. For smaller economies, for states already anchored in formal alliances, for states that chose sides early and publicly — the five-nation list is not a model. It is a verdict on choices already made, most of them irreversible.

The gap between those who understood this early enough to prepare and those now scrambling to catch up is not primarily a gap in intelligence or foresight. It is a gap in the willingness to accept, during years of apparent stability, that the architecture of access is more important than the architecture of alliance. Most states made the comfortable choice. The crisis has now priced that choice.

A Methodological Note

The five-nation list is not a clean dataset. It is revealed preference under stress, a combination of structural relationships built over years, immediate Iranian incentives in the first weeks of a war, and political signalling toward domestic and regional audiences simultaneously. Iran had reasons to grant access that had nothing to do with the recipient’s long-term positioning: Iraq shares a border and a religious majority; Pakistan is actively mediating; China’s economic weight makes denial structurally impossible. Reading the list too precisely risks overfitting to a single crisis artifact. What the list does provide, and what this analysis rests on — is a stress test: the moment when the relationships states had quietly accumulated were called upon, and either held or didn’t. The architecture matters. The list is the evidence, not the argument.

Follow on X: The Quiet Subscriber

Excellent analysis and clearly well-presented! A useful extension of this argument is that what we are witnessing is not just a shift from alliances to relationships, but a shift from security guarantees to access guarantees. For decades, states assumed that being inside a US-led security architecture would implicitly ensure continuity of trade and energy flows. The Hormuz crisis breaks that linkage. Security alignment did not translate into supply access when it mattered most. That forces a deeper recalibration. States will increasingly hedge not just militarily, but economically and diplomatically, building parallel channels of access even with adversarial actors. The emerging order, therefore, is not only multipolar, it is multi-aligned, where resilience depends less on who protects you and more on who will still transact with you under maximum pressure.

Another noteworthy analysis. Kudos!

Sir,

If it is a choice between leaning towards either the architecture of alliance or of access, where does that leave nations that are either small or do not have the wherewithals to invest in the access route?