The End of Monetary Unipolarity

Why the future of global finance may be defined by competing payment systems rather than a single dominant currency

The most important thing to understand about the future of the global monetary system is not which currency will replace the dollar. It is that no single currency is likely to replace it — and that China, the most plausible challenger, has strong structural reasons not to want the role.

This reframing matters because the dominant narrative — renminbi rises, dollar falls, monetary hegemony transfers — misunderstands how international monetary systems actually evolve. Reserve currency status is not simply a prize awarded to the largest economy. It is a structural burden that carries specific and severe costs. The country that issues the world’s primary reserve currency must supply liquidity to the global economy, which requires running persistent external deficits, opening capital markets, and accepting a degree of currency appreciation that undermines export competitiveness. For China, whose economic model is built on precisely the opposite set of dynamics, this is not an attractive proposition.

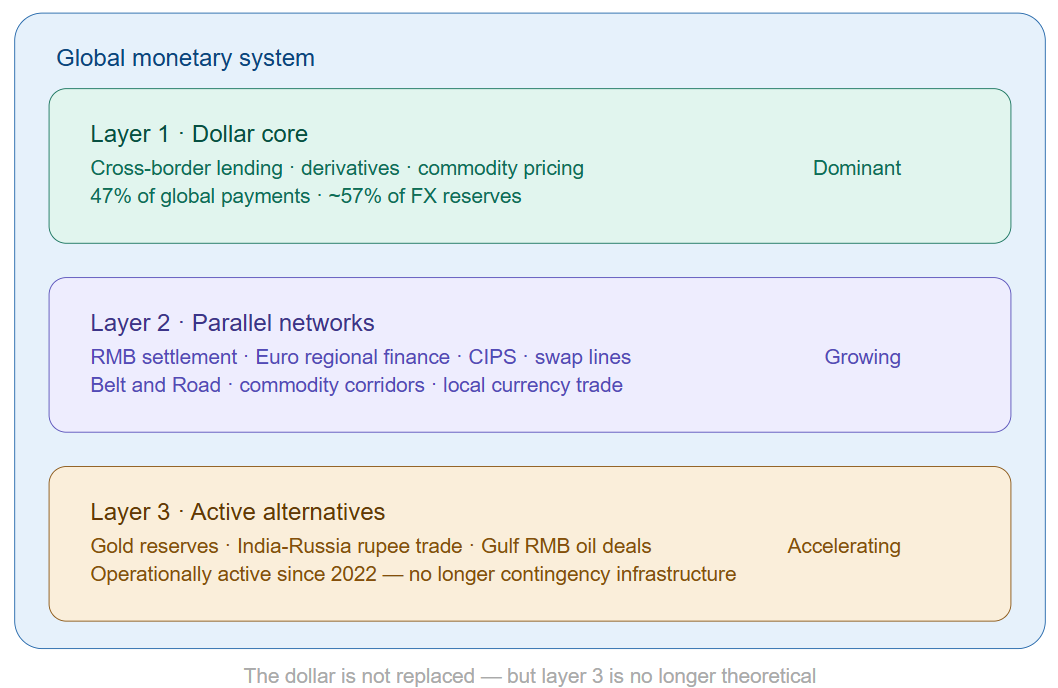

What is actually emerging is something more complex and more consequential than a simple hegemonic transition: a layered monetary architecture in which different currencies perform different functions across different networks of global trade and finance. The dollar does not get replaced. It gets supplemented — and in some domains, gradually circumvented. The defining feature of the next monetary era will not be replacement. It will be fragmentation.

Reserve currency status is not a prize awarded to the largest economy. It is a structural burden — and China has strong reasons not to want it.

The Triffin constraint: why dominance is a trap

The structural logic here was identified by economist Robert Triffin in 1960, and it has lost none of its relevance. The Triffin dilemma holds that a country issuing the world’s reserve currency faces an inherent contradiction: to supply the global economy with sufficient liquidity, it must run persistent current account deficits, exporting more financial assets than goods. Over time, this hollows out the domestic industrial base and creates structural imbalances that eventually undermine confidence in the currency itself.

The United States has lived with this constraint for seventy years. The dollar’s reserve status has conferred genuine advantages — the ability to borrow cheaply in its own currency, deep and liquid capital markets, and extraordinary geopolitical leverage, as demonstrated by the freezing of Russian sovereign reserves in 2022. But it has also required absorbing persistent trade deficits that have contributed to the deindustrialisation of significant parts of the American economy. The political backlash against that deindustrialisation — visible in successive administrations’ trade policies — is in part a consequence of the dollar’s reserve role.

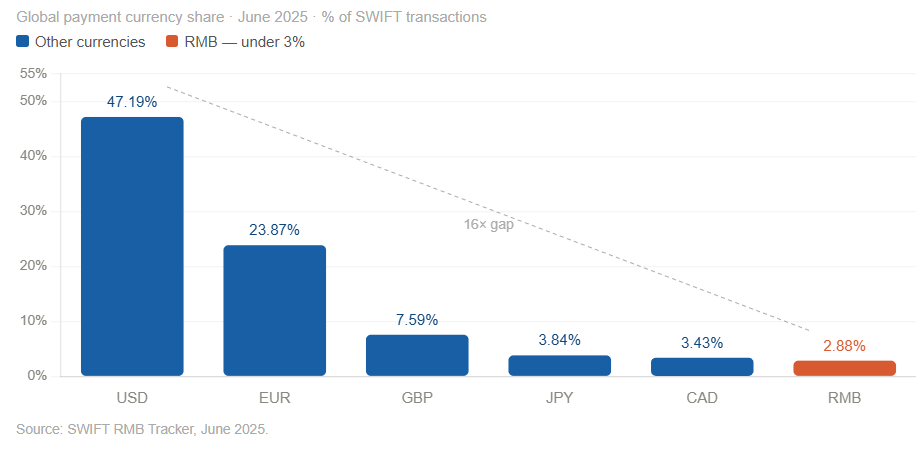

China’s policymakers understand this dynamic clearly. The renminbi currently accounts for under 3 percent of global payments, against the dollar’s 47 percent, according to SWIFT data from June 2025. That gap is not primarily a function of financial underdevelopment. It is a deliberate reflection of China’s preference for a managed currency, controlled capital flows, and a development model that prioritises export competitiveness over financial dominance. Abandoning those preferences to pursue reserve currency status would require China to accept the Triffin trap — and there is little evidence that Beijing considers that a worthwhile trade.

What China actually wants: autonomy, not dominance

The more accurate framing of China’s monetary ambitions is not replacement but insulation. The objective is to reduce vulnerability to the existing dollar-centred system rather than to displace it.

That vulnerability became acutely visible in February 2022, when Western governments froze approximately $300 billion of Russia’s sovereign foreign exchange reserves held in dollar- and euro-denominated assets. The action was legally unprecedented and geopolitically dramatic. For Beijing — which holds the world’s largest foreign exchange reserves, approximately $3.2 trillion as of early 2026 — the message was unmistakable: reserve assets held in a rival’s financial system are not politically neutral. They are a strategic exposure.

China’s response has been to accelerate the construction of parallel financial infrastructure that can operate independently of the dollar system when necessary. The Cross-Border Interbank Payment System, China’s alternative to SWIFT, processed approximately $12 trillion in transactions in 2024, up from $1.8 trillion in 2020 — a significant expansion, though still a fraction of SWIFT’s volume. Bilateral currency swap agreements between the People’s Bank of China and over forty central banks provide renminbi liquidity to trading partners without dollar intermediation. And in commodity markets, China has increasingly pushed for renminbi settlement: by 2024, approximately 25 percent of China’s oil imports were settled in renminbi, up from near zero in 2015.

None of these developments individually constitute a challenge to dollar dominance. Collectively, they represent the construction of a financial escape route — infrastructure that allows China and its trading partners to operate outside the dollar system if geopolitical circumstances require it.

China is not building a rival to the dollar. It is building an exit from the dollar’s reach — infrastructure that can operate independently when geopolitics demands it.

The sanctions shock and the search for redundancy

The Russian reserve freeze of 2022 was not just a bilateral action. It was a signal to every government that holds significant reserves in Western financial institutions: your assets are safe until they are not. The political conditions under which they cease to be safe are determined in Washington and Brussels, not in your own capital.

The response among non-Western central banks has been measured but directional. According to IMF COFER data, the dollar’s share of global foreign exchange reserves has declined from approximately 71 percent in 2000 to 58 percent in 2024 — a thirteen percentage point reduction over two decades. The pace of decline accelerated modestly after 2022. Gold purchases by central banks reached record levels in 2022 and 2023, with emerging market central banks — including China, India, Türkiye, and several Gulf states — accounting for the majority of buying. This is not de-dollarisation. It is diversification: the gradual acquisition of reserve portfolio redundancy.

The BRICS framework has provided institutional scaffolding for this diversification impulse, though its concrete achievements remain modest relative to its rhetoric. More significant in practice has been the bilateral dimension: China-Brazil trade settled in renminbi reached approximately $150 billion in 2023, roughly 30 percent of bilateral trade volume. India has conducted rupee-settled oil purchases with Russia. Gulf states have explored renminbi invoicing for Chinese energy sales. These are not system-threatening developments. But they represent the gradual normalisation of non-dollar settlement in trade flows that previously had no alternative.

The layered architecture: what it looks like in practice

The monetary system that is emerging from these dynamics does not resemble either the current dollar-centred order or the multipolar alternatives that analysts have been predicting for decades. It is more fragmented, more functional, and more geopolitically structured than either.

The dollar retains its central position in global finance — as the primary denomination for cross-border lending, derivatives, and commodity pricing, and as the safe asset of last resort. This is unlikely to change substantially in the medium term. The depth of U.S. capital markets, the liquidity of Treasury securities, and the network effects of dollar infrastructure are genuinely difficult to replicate. The dollar’s share of global payments at 47 percent, against the euro’s 24 percent and the renminbi’s 3 percent, illustrates how far any challenger remains from parity.

But alongside this dollar core, a series of parallel networks is developing. The renminbi is expanding its role in trade settlement within China’s economic orbit — particularly across the Belt and Road network, in commodity transactions, and in bilateral trade with partners who have reason to reduce dollar exposure. The euro maintains its position as the second global currency, with particular strength in European neighbourhood trade and bond markets. And at the margins, regional currencies are gaining ground in specific bilateral corridors.

What is emerging, in other words, is functional specialisation: different currencies performing different roles in different parts of the global economy, with the dollar remaining dominant in global finance while its role in trade settlement gradually diversifies. This is not the end of dollar hegemony. It is the beginning of dollar non-exclusivity.

The costs of fragmentation

It would be analytically incomplete to describe this transition without acknowledging its costs — and they are real.

A fragmented monetary system is less efficient than a unified one. When trade is settled in multiple currencies rather than one, transaction costs increase, hedging requirements multiply, and the pricing of cross-border risk becomes more complex. The efficiency gains from monetary unipolarity — the reduction in transaction costs that a single dominant currency provides — are not trivial. Estimates vary, but the dollar’s role as a vehicle currency is estimated to reduce global transaction costs by several hundred billion dollars annually. Fragmentation erodes that benefit.

Fragmentation also creates new instabilities. In a world of competing financial infrastructures, financial crises can propagate in less predictable ways. The 2008 crisis spread rapidly because of the dollar system’s integration; a fragmented system might contain crises more effectively in some scenarios but create new transmission channels in others. The interaction between dollar-denominated debt in emerging markets and renminbi-denominated trade settlement, for instance, creates currency mismatches that did not previously exist at scale.

And fragmentation creates strategic complexity. A world of competing payment systems is also a world of competing financial sanctions regimes, competing regulatory standards, and competing reserve asset classes. The geopolitical management of a multipolar monetary system is substantially more demanding than the management of a unipolar one — for all parties, including those who believe they benefit from the transition.

What to watch

Several signals will reveal whether the shift toward monetary multipolarity is accelerating or stabilising. Currency usage in energy and commodity trade is the most sensitive indicator: energy markets have historically reinforced dollar dominance, and any sustained shift toward renminbi or other currency invoicing in oil and gas transactions would represent a structural change in the architecture of global trade finance.

The relative growth of CIPS versus SWIFT — measured not just in transaction volume but in the number and type of institutions connecting — will indicate whether parallel financial infrastructure is becoming genuinely systemic or remaining a niche alternative. Central bank reserve composition, tracked quarterly through the IMF’s COFER database, will reveal whether the post-2022 diversification trend is sustained or mean-reverting. And the trajectory of dollar-denominated debt in emerging markets will show whether the liabilities side of the global balance sheet is diversifying as fast as the assets side — a divergence that, if it persists, creates exactly the kind of currency mismatch that makes fragmentation dangerous rather than merely expensive.

None of these indicators alone signals a definitive transition. But together they will trace the contours of the monetary system that is actually emerging — which is likely to be more complex, more contested, and more costly to navigate than either the current order or its predicted successors.

Conclusion

The question most analysts ask about the future of the dollar is the wrong one. The world is not waiting for a successor currency. It is building workarounds — parallel infrastructure, bilateral settlement arrangements, and reserve diversification strategies — that reduce dependence on the existing system without replacing it.

China does not want dollar-style dominance, and the Triffin dilemma explains why. What it wants — and is systematically building — is the capacity to operate outside the dollar system when geopolitical conditions make dollar exposure strategically unacceptable. Other states, watching the Russia reserve freeze, are drawing similar conclusions about the value of financial redundancy.

The result is not a new monetary hegemon. It is a layered, fragmented, and geopolitically structured monetary architecture in which the dollar remains the dominant pillar but is no longer the only one. That transition carries real costs — in efficiency, in stability, and in the complexity of managing a system with no single centre of gravity.

The end of monetary unipolarity is not a moment. It is a process. And it is already underway.

Follow on X: The Quiet Cartographer