Kharg Island: The War Has Entered the Energy System

How a single export node turned a regional strike into a global systems shock

There are moments when a place stops being a place. It becomes a signal.

Kharg Island is one such place. A small coral outcrop, 25 kilometres off Iran’s southwestern coast, surrounded by deep water, connected by subsea pipelines to the giant oilfields of Khuzestan. For decades it sat at the centre of Iran’s export economy without attracting much attention outside specialist circles. That changed on 28 February 2026, when US and Israeli strikes on Iran brought it to the top of every energy market briefing on the planet.

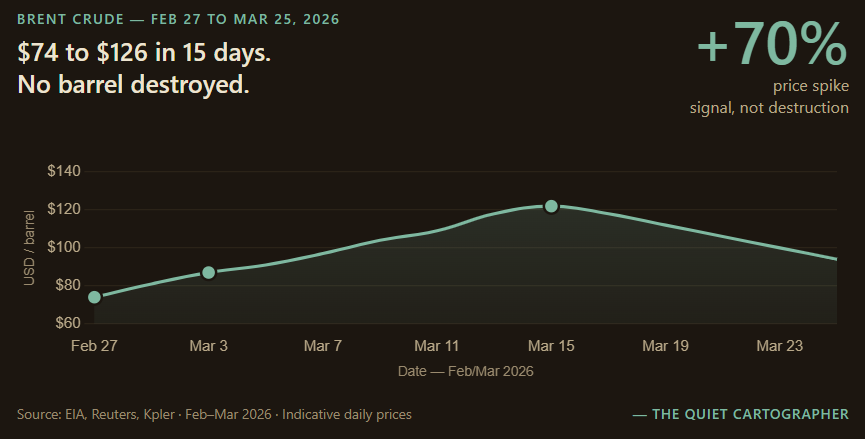

The strikes hit military installations — runways, missile bunkers, mine storage. The oil infrastructure was left untouched, deliberately. And yet within days, tanker traffic through the Strait of Hormuz had dropped by more than 70%. Insurance premiums for a single strait transit surged from $100,000 to over $400,000 for a large tanker — a 300% increase in weeks. Brent crude crossed $100 per barrel by 8 March for the first time in four years, climbing to $126 at its peak.

Kharg’s oil facilities had not been hit. The disruption happened anyway. This is the part that matters: The island was not destroyed.

The geometry

To understand why, we need to understand the structure of Iran’s oil system — not its scale, but its geometry.

Iran’s crude export infrastructure is not a dispersed web. It is a funnel. Oil is extracted from fields concentrated in Khuzestan province — which alone produces roughly 70% of Iran’s crude — moved through inland pipelines, and consolidated at a handful of terminals for export. Of those terminals, one dominates everything else.

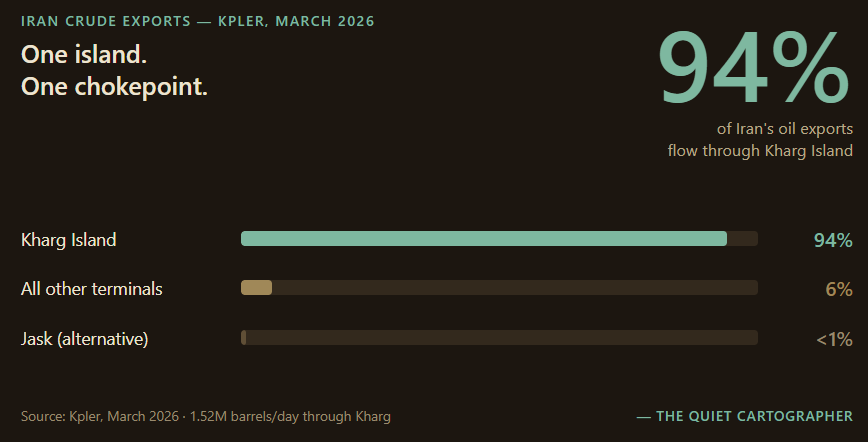

According to Kpler data covering the past twelve months, 94% of Iran’s crude exports — approximately 1.52 million barrels per day — departed from Kharg. The island handles roughly 90% of Iran’s total oil export revenues. Iran earned approximately $78 billion from energy exports in 2024 despite heavy sanctions; the majority of that revenue flows through a single coral outcrop in the northern Persian Gulf.

Iran is aware of this vulnerability. In February 2026, in the weeks before the strikes, Tehran ran its export rate to nearly three times the normal pace — close to 4 million barrels per day according to Kpler — drawing down storage from 27 full tanks to 9 in preparation for what was coming. The front-loading was a signal too: a country preparing for the moment its main financial artery might be cut.

What emerges is a system optimised for efficiency that has made itself maximally exposed to precision. When flow is this concentrated, disruption does not need to be widespread. It only needs to be precise. Remove Kharg from the equation and upstream production does not gradually decline — it becomes temporarily irrelevant. Oil that cannot be exported is, in economic terms, oil that does not exist.

Available supply is not the same as accessible supply

The day the strikes began, Kharg’s loading operations continued. Tankers kept arriving. By some accounts, loading ran non-stop through the first days of the conflict. Iran’s oil infrastructure had not been destroyed.

And yet the market responded as if it had.

This is a distinction that rarely gets made explicit, but it sits at the centre of how modern energy systems actually fail. The question is not how much oil exists. The question is whether it can be processed, moved, insured, and delivered.

Kpler noted within days of the strikes that the Strait of Hormuz was effectively closed for commercial shipping — not because Iran had physically blocked it, but because insurance withdrawal had done the work. For a ship operator, a strait transit without war-risk coverage is not a business decision. It is an existential one. Most simply stopped sailing. By early March, tanker traffic in the region had fallen from around 130 ships per day to single digits.

This is what a functionality shock looks like — as distinct from a supply shock.

A supply shock is what most energy disruption analysis is built around: a field goes offline, output drops, prices adjust. The system, while stressed, remains intact. Markets find substitutions. Strategic reserves get released. The IEA announced the largest-ever coordinated reserve release — 400 million barrels — within days of the strikes.

A functionality shock is different in kind, not degree. When midstream and downstream infrastructure are simultaneously affected — through insurance withdrawal, route closure, tanker hesitation, or actual damage — the question is no longer how much energy exists but whether it can move. A functioning gas field connected to a disrupted pipeline is not producing. A full storage tank connected to a closed strait is not exporting. The mechanisms that enable substitution are themselves disrupted.

Iran has an alternative export terminal — Jask, on the Gulf of Oman, designed precisely to bypass Hormuz. In the first two weeks of March 2026, it handled one cargo of roughly 2 million barrels. By comparison, Kharg handles 1.5 to 2 million barrels on a normal day. The backup route exists. It cannot carry the load.

The cascade

Here is what actually happened in the four weeks after 28 February 2026, and why it matters beyond the oil price.

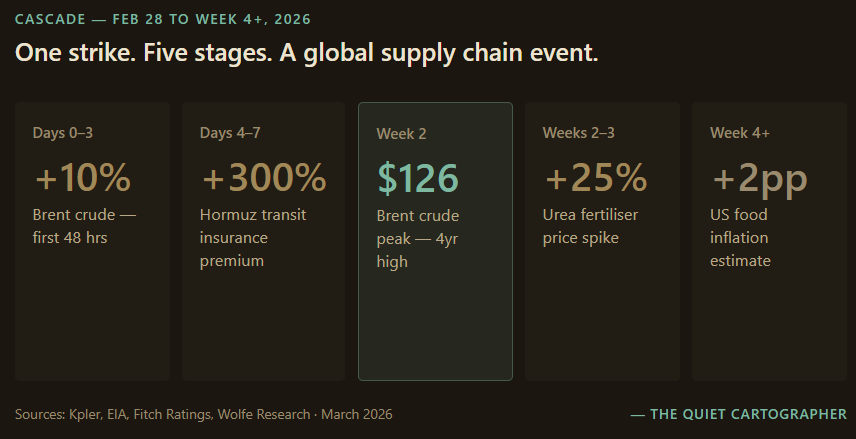

Days 0–3. Strikes on Iranian military infrastructure. Oil operations at Kharg continue. Insurance premiums for Hormuz transit begin climbing. Maersk, Hapag-Lloyd, CMA CGM suspend regional operations. Brent crude rises 10% in the first 48 hours.

Days 4–7. Iran declares the Strait closed to US, Israeli, and allied-flagged vessels. At least five tankers struck. Around 150 ships anchor outside the strait. Tanker traffic falls to near zero. Brent surpasses $100 per barrel by 8 March — the first time since 2022. Qatar pauses LNG production at Ras Laffan and Mesaieed following drone strikes. European natural gas futures jump 30% overnight. LNG freight rates surge more than 40%.

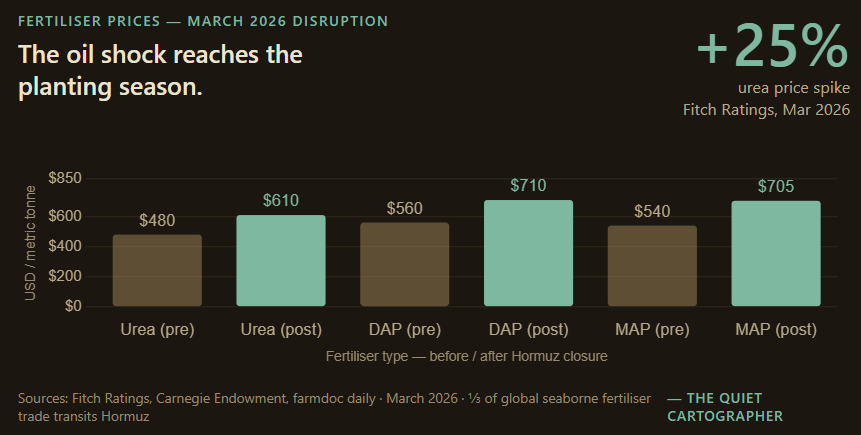

Weeks 2–3. The disruption begins moving beyond energy markets. About one-third of global seaborne fertiliser trade passes through the Strait. The effective closure cuts fertiliser exports from Gulf producers — among the world’s largest — at the worst possible moment: the start of the Northern Hemisphere planting season. Urea prices spike from around $480 per ton before the war to above $600 by mid-March. DAP and MAP breach $700 per ton. Fitch Ratings raises 2026 ammonia and urea price expectations by 25%, warning of further increases if the closure persists.

Week 4 and beyond. American farmers unable to lock in nitrogen prices ahead of spring planting. More than 50 agricultural groups write to the White House calling for emergency relief. Wolfe Research estimates the disruption could add roughly 2 percentage points to US food-at-home inflation. UNCTAD warns that developing countries — particularly in Africa and South and Southeast Asia — face the most acute long-term exposure. The Dallas Fed models a 1.3 percentage point reduction in global GDP growth if the disruption persists for three quarters.

This is what the feedback document called “scheduled stress.” The oil price spike is visible and immediate. The fertiliser shortage arrives at the planting window and will be felt in harvests months from now. The food price consequences reach consumers later still. The cascade does not announce itself all at once.

The escalation constraint — and its limits

Given Kharg’s importance, it appears to be an obvious target. And yet as of late March 2026, its oil infrastructure remains untouched.

The reason is not goodwill. It is constraint.

Disrupting Kharg’s oil facilities is not a contained tactical move. It is an action that reverberates through the entire global energy system — affecting not just Iran but every economy that depends on what flows through the Persian Gulf. Senior officials within the Trump administration have publicly discussed the option. The restraint is not absence of intent. It is calculation of cost.

That cost is structural. If Kharg’s oil infrastructure were seriously damaged, Kpler’s senior crude oil analyst estimates it could take Iran months, if not over a year, to rebuild — a country operating under western sanctions, unable to secure the financing, technology, or expertise needed for rapid reconstruction. The long-term removal of 1.3 to 1.5 million barrels per day from global supply would place markets under sustained pressure at a moment when alternative routes are already strained.

But this constraint has a harder edge than is usually acknowledged. The historical record shows that critical nodes do get targeted when actors decide the cost is worth paying. Kharg itself was bombed repeatedly during the Iran-Iraq War in the 1980s. Iraq calculated, correctly, that the disruption to Iran’s revenue outweighed the geopolitical cost. Iran repaired the facilities and resumed exports — but the damage was real and the calculation was made.

The constraint delays action. It does not eliminate it. The more accurate formulation is this: the higher the cost of targeting a node, the more pressure must accumulate before that threshold is crossed. What we are watching in March 2026 is a system operating close to that threshold — not yet over it, but closer than at any point in decades.

The actors you don’t see

The United States has been explicit about its presence. US administration has discussed offering war-risk insurance to tankers to keep traffic moving. The strategic logic is not humanitarian — it is structural. American influence in the Gulf has always been tied as much to ensuring energy flow as to any other objective. A Hormuz that cannot be kept commercially navigable is a fundamental challenge to that role.

China’s position is less visible but no less consequential. As of 2025, China imported roughly 1.5 million barrels per day from Iran through Kharg alone, making it overwhelmingly the largest buyer of Iranian crude. Kpler estimates that more than 200 million barrels of Iranian crude are currently stored on tankers near China — roughly five months of supply — a buffer built in anticipation of exactly this kind of disruption. Deliveries to China have edged higher since tensions escalated, not lower.

China has not intervened directly. It has not needed to. Its structural exposure — and the size of that floating reserve — operates as background pressure on the boundaries of escalation. Any action that threatens sustained disruption to Iranian oil flows threatens China’s most reliable low-cost energy source. That exposure does not produce overt intervention. It produces a gravitational constraint on how far the conflict can go before it starts costing actors who are not currently fighting.

Power, in this sense, is not always exercised through action. It is often expressed through constraint.

Functionality, not territory

The deeper shift that Kharg illustrates goes beyond Iran, beyond this particular conflict, beyond oil.

Across the Middle East since 28 February 2026, energy infrastructure has been targeted as a deliberate instrument — not as collateral damage but as strategy. Drone strikes on Qatari LNG facilities at Ras Laffan. Attacks on fuel storage in Tehran and the Alborz region. Drone strikes on the Omani ports of Duqm and Salalah, which had been positioned as alternative routes around a closed Hormuz. The Joint War Committee of the London insurance market added waters around Oman to its list of high-risk areas within days.

The logic is consistent. Targeting energy systems allows pressure to be applied without occupying territory. It degrades the opponent’s ability to function rather than attempting to control it directly. It operates within interconnected global systems, so its effects spill outward — into insurance markets, supply chains, food prices, and the political calculations of countries that are nowhere near the conflict zone.

This does not replace traditional forms of warfare. It overlays them. What changes is the geography of consequence. A drone strike on a gas terminal in Qatar raises heating costs in South Korea. A closure of the Strait of Hormuz threatens the planting season in Iowa. An insurance withdrawal from a maritime zone removes barrels from a market in which every economy participates.

The conflict is regional. The system is global. And the system does not distinguish between combatants and dependents.

The pattern beyond Kharg

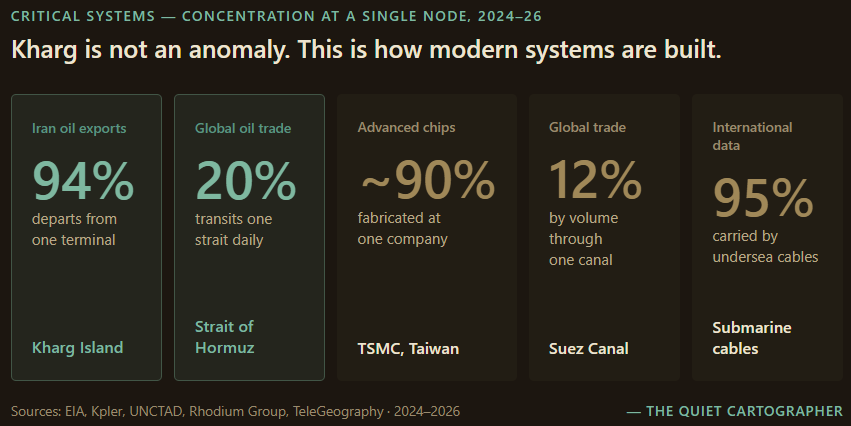

Kharg is not unique. It is simply visible.

Across the global system, similar points of concentration exist — places where flow is consolidated for the sake of efficiency until the efficiency itself becomes the vulnerability. The Strait of Hormuz carries approximately 20 million barrels of oil per day — about one-fifth of global supply — and around 20% of global LNG. TSMC’s facilities in Taiwan fabricate the majority of the world’s most advanced semiconductors. The Suez Canal handles roughly 12% of global trade. Undersea cable networks carry more than 95% of international data.

Each represents the same trade-off: optimise for throughput, accept concentration, create a point where disruption does not need to be widespread to be effective — it only needs to be precise.

In a more stable world, that trade-off makes rational sense. In a world defined by strategic competition and the deliberate targeting of systems rather than territory, it becomes progressively harder to sustain.

The strategic implication

The map of power is no longer drawn primarily in borders or territories. It is drawn in bottlenecks.

But there is a further step that the Kharg moment forces into view. If bottlenecks define where systems are most exposed, then the strategic asset that matters most is no longer production capacity. It is resilience — the ability to absorb a node-level disruption without cascading failure.

Saudi Arabia can reroute crude through its East-West pipeline to the Red Sea port of Yanbu. The UAE can divert oil through the Abu Dhabi Crude Oil Pipeline to Fujairah. These alternatives exist precisely because both countries recognised, over decades, that Hormuz dependency was a vulnerability. The pipeline infrastructure cost billions to build and serves as strategic insurance.

Iran has no equivalent. Jask was meant to be that insurance. It cannot carry the load. The result is a country whose entire export capacity runs through a single island terminal that a CIA document in 1984 already described as “the most vital in Iran’s oil system, and their continued operation is essential to Iran’s economic well-being.” Forty years later, nothing structural has changed.

The lesson is not specific to Iran. It is a systems principle. Optimisation without redundancy is not a stable state — it is a deferred crisis. And the longer a system runs without being tested, the more invisible that fragility becomes.

What the current disruption makes visible — for anyone building infrastructure, managing supply chains, or assessing strategic risk — is that the question has changed. The question is no longer: how much can this system produce? It is: what happens when the point through which everything must pass stops working?

Because when energy systems are the battlefield, the effects are not limited to those who are fighting.

They extend, in stages and with delay, to those who depend on them.

Follow on X: The Quiet Cartographer

Sources and suggested reading:

Kpler (Iran crude export data, March 2026)

Iran Open Data Center

EIA (Strait of Hormuz transit data, 2024–2025)

Wikipedia — 2026 Strait of Hormuz crisis

UNCTAD — Strait of Hormuz disruptions report, March 10 2026

IFPRI — Iran war food security impacts, March 2026

farmdoc daily — Fertiliser supply risks, March 17 2026

CNBC — fertiliser prices, March 11 and March 25 2026

Carnegie Endowment — fertiliser and food crisis analysis, March 2026

Fortune — fertiliser shortage analysis, March 24 2026

Dallas Fed — Hormuz closure economic modelling, March 20 2026

Stimson Center — global markets and Hormuz, March 2026

Kpler — US-Iran conflict market analysis, March 1 2026

ABC News, CNN, Al Jazeera, Ynet News — Kharg Island reporting, March 2026.

Great piece. The GCC workarounds have the same limitations as the Iranian one, they can’t handle the load. I would also flag that some of the restraint around attacking energy infrastructure on Kharg has to do with the fact that Iran would then effectively destroy GCC infrastructure, taking way more than 1.5 million barrels offline for much longer. In addition, forces in Yemen are on standby to close off the Red Sea access point if it becomes necessary.

The functionality shock framing is the right distinction and it's underused.

What you describe at Kharg extends further: Iran has now demonstrated it can monetise the functionality gap rather than just exploit it. Charging $2mn per transit converts a disruption into a revenue model.

The strait doesn't need to reopen for Iran to benefit, it just needs to remain selectively functional. That changes the incentive structure permanently.