India's Next Bottleneck Isn't Capital — It's Electricity

India built the capacity. It didn't build the system to deliver it.

India’s electricity problem is not a shortage. It is a coordination failure. And coordination failures cannot be solved with capital alone.

That distinction has moved from analytical to operational in the past year. In March 2026, India’s LPG carriers transited a partially closed Strait of Hormuz under direct diplomatic clearance from Iran, while Washington issued a 30-day waiver, reflecting its uneven response to India’s ongoing purchases of discounted Russian crude. India managed its external energy exposure through active diplomacy as its physical infrastructure — distribution networks, storage capacity, grid resilience — offered limited buffer against a prolonged supply shock. The diplomatic architecture held. However, it revealed the underlying fragility it was compensating for.

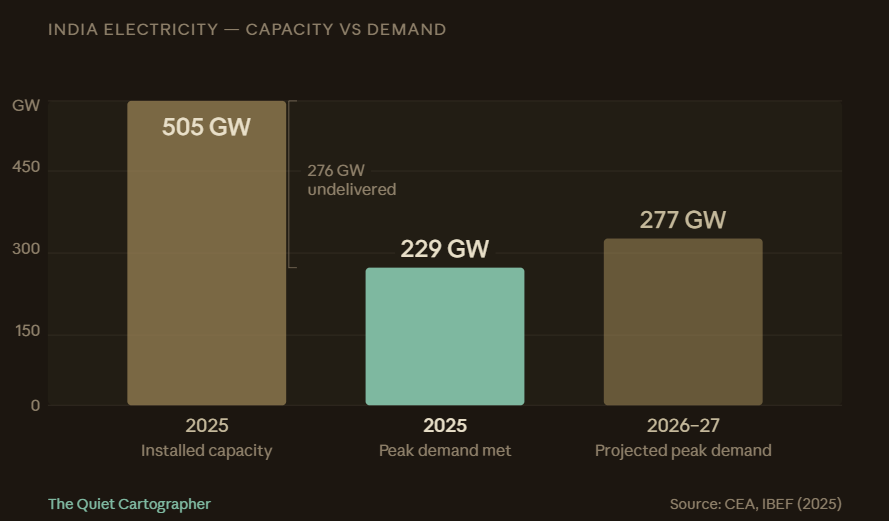

Electricity is that fragility in its most concentrated form. India has 505 gigawatts of installed capacity. It meets 229 gigawatts of peak demand. That gap — capacity that exists but cannot be reliably delivered — is the clearest signal of where the growth constraint has moved. The country does not lack power. It lacks the ability to synchronise what it has built with what its economy needs, where it needs it, when it needs it.

From Scarcity to Expansion to System Stress

India’s electricity system has evolved across three distinct phases, and understanding the transition between them is the key to understanding where the constraint now sits.

The first phase was scarcity. Power shortages constrained industrial output. Outages were routine. The binding constraint was simple: not enough capacity existed.

The second phase was expansion. From the mid-2000s onward, India scaled aggressively. Generation capacity rose from roughly 130 GW in 2005 to over 500 GW by 2025. Transmission networks expanded. Electrification deepened across states and sectors. This solved the visible constraint of the first phase. It created a less visible one.

As systems scale, coordination becomes harder than expansion. The constraint shifts from building capacity to aligning generation, transmission, distribution, and demand across a system that is no longer internally contained or simply managed. India is now in that third phase — defined not by shortage but by system stress.

The gap in Visual 1 is the argument. India has built well beyond current peak demand. This is not excess power in a usable sense. A significant share of installed capacity is intermittent, geographically misaligned, or unavailable at peak—turning apparent surplus into operational stress. The constraint is not the quantity of power — it is the system's ability to deliver it reliably, at the right location, under the conditions of an increasingly complex and volatile demand profile.

Demand Is Changing Shape — And Breaking Old Assumptions

Electricity demand is no longer a smooth function of GDP growth. It is being reshaped by sectors that behave fundamentally differently from traditional industrial loads — and that the grid was not designed to serve.

Data infrastructure is one of the clearest examples. India’s data centre capacity is projected to reach approximately 3.4 GW by 2030, driven in significant part by AI workloads that create continuous, high-density demand with zero tolerance for interruption. Electric mobility introduces localised spikes — charging demand clusters in urban zones and along transport corridors, stressing distribution networks rather than the system as a whole. Cooling demand is becoming structural, already accounting for roughly 7 percent of electricity consumption and rising with income levels and heat intensity.

The grid is no longer managing predictable load growth. It is managing concentrated, volatile, and operationally rigid demand — from sectors that scale fastest in precisely the locations where the grid is most stressed.

Where the System Starts to Break

The stress emerges at three points where system components fail to align. They are not equal, and treating them as equivalent obscures which problem is actually binding.

Transmission is the first fault line. Renewable capacity is increasingly concentrated in Rajasthan, Gujarat, and Tamil Nadu, while demand is concentrated in industrial and urban centres elsewhere. Transmission build-out has lagged this geographic shift, leading to rising renewable curtailment and underutilised assets. India plans to invest over ₹9.15 lakh crore in transmission infrastructure by 2032. The constraint is not intent. It is execution speed relative to system needs — and whether investment can close a gap that widens as renewable deployment accelerates.

Renewable intermittency is the second fault line. Solar and wind capacity are expanding rapidly, but peak generation does not align with peak demand. Storage remains costly at scale. The result is counterintuitive: rising system costs despite falling generation costs. Power is curtailed during periods of excess supply and supplemented by expensive thermal backup during deficits. The system pays simultaneously for overcapacity and under-capacity — at different times of day and in different parts of the country.

There is a structural dimension to this fault line that most analysis understates. India’s renewable transition depends heavily on imported solar modules, battery technologies, and upstream supply chains concentrated primarily in China. At current deployment rates, India will substitute a crude oil import dependency for a clean energy component dependency — with a supply chain that is no less geographically concentrated and considerably less diplomatically manageable. The Hormuz episode demonstrated what happens when an external supply chain is disrupted and internal redundancy has not been built. India’s renewable build-out is replicating that exposure in a different register.

Strategic autonomy in energy cannot be achieved by exchanging one structural dependency for another — it requires building the domestic manufacturing base that makes the transition genuinely self-sustaining. India’s solar module production capacity, while growing, remains well behind its installation targets. That gap is a strategic liability, not just an industrial policy question.

Distribution is the third fault line — and the deepest one. This is not a technical coordination problem with a known engineering solution. It is a structural constraint embedded in governance, and it transmits inefficiency across the entire system regardless of what is built above it.

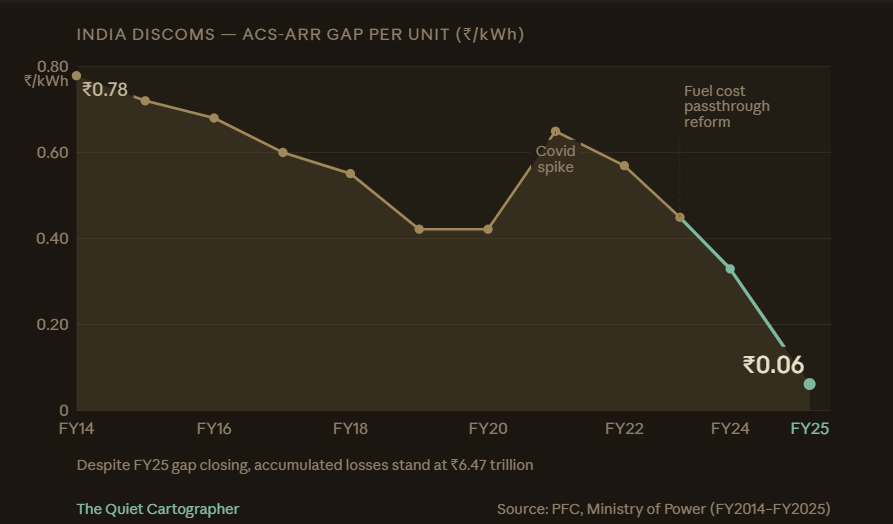

India does not operate a single electricity system. It operates multiple state-level systems governed by fragmented and misaligned incentives. Distribution companies — DISCOMs — remained financially stressed for over a decade. Tariffs were politically determined rather than cost-reflective. Agricultural and residential users were subsidised. Industrial users cross-subsidised the system, raising their costs and compressing competitiveness. Payment delays cascaded upstream, weakening generators and transmission operators who could not plan or invest on the basis of receivables that might not materialise.

The gap between the average cost of supply and average revenue did not persist unchanged—it narrowed—but it did not resolve. Each reform cycle reduced it temporarily without removing the underlying political constraint: tariffs are easier to defer than to correct, and state governments remain unwilling to impose cost-reflective pricing on voters.

What changed was not political will — it was a technical workaround. The 2022 fuel cost passthrough reform allowed DISCOMs to automatically recover rising power procurement costs rather than waiting years for tariff revisions. Smart metering improved billing accuracy.

By FY2025, the ACS-ARR gap had narrowed to to near-zero levels, and DISCOMs recorded a collective profit for the first time in over a decade.

This is real progress. It should not be dismissed.

But it is progress built on a workaround, not a resolution. The accumulated losses of Indian DISCOMs still stand at ₹6.47 trillion — a legacy of the decade in which the gap held. Free agricultural power remains politically untouchable in most states. Cross-subsidies that raise industrial tariffs and suppress manufacturing competitiveness persist. The draft Electricity Amendment Bill, 2025, promises to introduce retail competition and address these structural distortions — but it has not yet been presented to Parliament, and its contradictory commitments to both eliminating cross-subsidies and fully protecting farm and low-income tariffs have yet to be reconciled.

The fuel cost passthrough closed the pricing gap. It did not reform the political economy that created it. Until that layer is addressed, the system remains one policy reversal away from the conditions that produced a decade of losses — and the ₹6.47 trillion in accumulated debt that still sits on the balance sheets of the utilities that distribute power to ninety percent of India’s electricity consumers.

Electricity as Filter

The cumulative effect of these three fault lines is not a crisis. It is a filter.

Capital does not wait for systems to stabilise. It moves to where they already are stable. Investment clusters in regions with reliable, cost-reflective electricity. Industrial geography shifts accordingly. Sectors that depend on continuous, high-quality power — data infrastructure, advanced manufacturing, pharmaceutical production — locate where supply is dependable, not where policy intent says it should be. Other regions fall behind, regardless of announced targets.

This filtering mechanism is already operating. High-growth urban clusters face rising power costs or localised reliability constraints. Renewable-heavy regions experience curtailment alongside peak shortages. Distribution networks strain under localised overloads from EV adoption and cooling demand. The system is not failing uniformly — it is sorting the economy spatially and sectorally, in ways that compound over time.

Electricity has become a selection mechanism. It determines which parts of the economy expand efficiently and which do not. It shapes industrial geography. It filters capital allocation. And it does so without announcing itself — not as a headline crisis, but as a persistent drag that makes the growth model less productive than the capacity numbers suggest it should be.

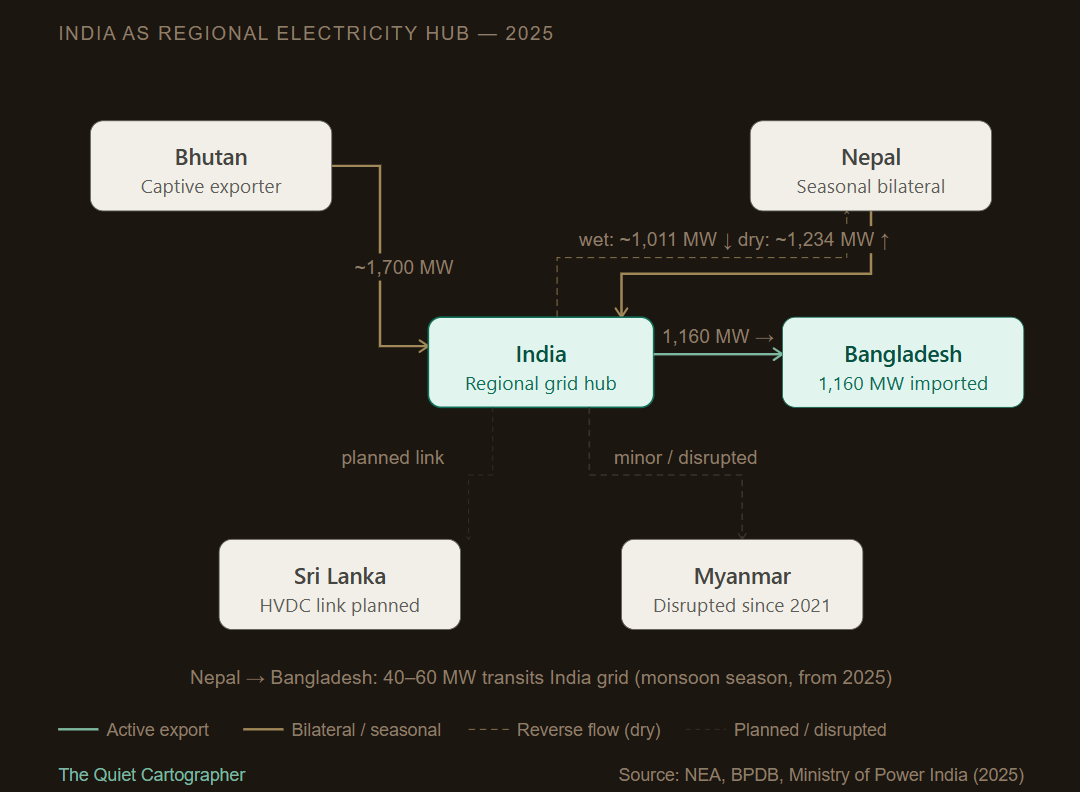

The filter does not stop at India’s border. Bangladesh imports approximately 1,160 MW of electricity directly from Indian generators through dedicated cross-border transmission lines — roughly 8 percent of its peak demand — with expansion agreements that assume continued Indian supply reliability. Nepal’s deepening cross-border transmission integration places it in a similar position of seasonal reliance on Indian grid balancing for periods when its own hydropower generation falls short. For these economies, India’s internal coordination failures are not a distant policy question. They are an operational reality: when Indian DISCOMs delay payments upstream, when transmission constraints limit exportable surplus, or when peak shortages force India to prioritise domestic supply, the downstream effects cross borders without announcement. The same coordination constraints that shape power availability within India also condition how reliably surplus can be exported across borders—though mediated through bilateral agreements and grid priorities rather than direct market transmission. India’s electricity system was built as national infrastructure. It now functions — incompletely and without deliberate design — as regional infrastructure. The gap between those two things is where the next set of vulnerabilities sits.

The Constraint That Matters Now

India does not lack the ambition, the capital access, or the technical knowledge to build a world-class electricity system. What it lacks is the political will to reform the layer of the system where the deepest failure sits.

Transmission investment can be accelerated. Renewable capacity will continue to expand. Storage costs will continue to fall. These are tractable problems on known trajectories.

The DISCOM problem is different. It cannot be engineered around. Every investment made above it — in generation, in transmission, in storage — flows through a distribution layer that prices power incorrectly, pays its suppliers late, and cross-subsidises consumption in ways that distort the entire system. Until that layer is reformed, the system will continue to produce the same outcome: capacity that cannot be delivered reliably, investment that underperforms its potential, and growth that is slower and more uneven than it should be.

India’s electricity system is no longer defined by how much capacity it can add. It is defined by whether it can govern what it has already built. If it cannot, the constraint will not announce itself as a shortage. It will operate as a filter — selecting which sectors and regions get to scale, and which do not.

That is a harder problem to fix than building more power plants. And, unlike capacity expansion, it cannot be solved with capital alone.

Follow on X: The Quiet Cartographer

Sources and Additional Reading:

Average tariff hike of 4.5 per cent needed to eliminate ACS-ARR gap, notes ICRA

Central Electricity Authority - Installed Capacity Report 2026

Two reforms that rewired the India’s electricity distribution sector

The shift from capital to electricity as the binding constraint is the right diagnosis. The next layer down is which electricity — grid-connected, captive, or open-access. Industrial users are already routing around the grid through captive solar plus storage. The bottleneck moves from generation to the open access approval queue and the feeder-level reliability that determines whether that bypass is worth building.

Because China’s power system is roughly twenty years ahead of India’s, I would add several points based on China experience.

This post argues that India’s main electricity constraint is no longer insufficient installed capacity, but coordination failure. On the surface, installed capacity has risen far above peak demand. But that capacity still cannot be delivered at the right time, in the right place, and with the reliability required by the sectors that actually need power. As a result, the binding growth constraint is shifting from “building more power plants” to “actually coordinating generation, transmission, distribution, and demand into a functioning system.”

In my view, there are several points need to consider again:

First, the article deliberately reframes the problem from “shortage” to “coordination,” but India has not yet reached a stage where electricity is truly abundant and merely poorly delivered. The apparent surplus implied by 505GW of installed capacity against 229GW of peak demand does not automatically mean India has escaped supply constraints. Installed capacity is a broad statistical category that includes large volumes of low-utilization, non-dispatchable, seasonally volatile, maintenance-constrained, or fuel-limited capacity. In other words, nameplate capacity is not the same thing as reliably deliverable power.

A comparison with China makes this even clearer. China’s installed capacity is now around 3,900GW (see the chart I made below), while peak load is roughly 1,450GW, a ratio of about 2.7x. India’s comparable ratio is only around 2.2x. By that standard, India’s installed capacity is still far from ample. Moreover, over the past decade, India’s power capacity has grown faster than that of most Western economies, but it has still expanded by only about 60%, whereas China’s installed capacity increased by roughly 1.4 times over the same period. So the Indian problem is not simply that power is being coordinated badly. The system is also still underbuilt relative to the scale of what India ultimately wants its economy to become.

Second, on transmission, the article is right to identify the spatial mismatch. Renewable energy is concentrated in places such as Rajasthan, Gujarat, and Tamil Nadu, while demand is concentrated elsewhere, producing renewable curtailment and underutilized assets. This pattern is very similar to China’s. In my earlier post, Ultra-High Voltage: China’s Most Underrated “Energy Logistics Technology,” I discussed how China addressed exactly this problem. In China, more than 80% of energy resources are concentrated in the western and northern regions, while over 70% of energy consumption sits in the east and central regions. Distances between resource-rich areas and load centers often run from 1,000 to 4,000 kilometers. This spatial mismatch implies a simple truth: in China, the core task of the power system is not only to generate electricity, but to deliver it to where it is needed. That is why more than 90% of the world’s UHV transmission lines are in China. India is running into a structurally similar challenge, but without yet possessing transmission infrastructure on anything like that scale.

Third, on renewable intermittency, this is not an India-specific problem at all. It is a global one. The core issue is that renewable generation does not align perfectly with peak demand, while storage remains expensive, so the system is forced to curtail power during periods of excess supply and rely on costly thermal backup during periods of shortage. There is only one real long-term solution: massive deployment of energy storage. That is exactly why China now accounts for more than 90% of global energy storage production and sales. Without large-scale storage, no country can truly solve the intermittency problem. It can only shift the burden around within the system.

Finally, I would say that the article goes too far when it compares India’s dependence on China for renewable components, storage systems, and upstream clean-energy supply chains with the vulnerability exposed by the Strait of Hormuz in fossil-fuel imports. That analogy overextends the concept of national security. China did not achieve its current global dominance in transmission, distribution, and storage by sealing itself off. Quite the opposite. Decades ago, China actively embraced Western capital, imported Western equipment and technology, and allowed Western multinationals to earn enormous profits in the Chinese market. Only after decades of absorption, learning, scaling, and system-building did China reach its current level.

So if India now tries to wall itself off, or insists on obtaining Chinese capital and technology without Chinese influence or control, it is hard to see how it can solve these problems on its own. I discussed this issue in another post, India Wants Chinese Money & Tech Without Chinese Control. Can That Model Work?If India wants a world-class power system, it cannot rely on strategic hesitation, political fragmentation, and technological defensiveness. It has to decide whether it truly wants system-building — and system-building always begins with openness, scale, and learning.