How Britain Built a Self-Sealing Political Economy

Britain's experience offers a warning for economies where asset wealth has outpaced productive growth

Britain’s problem is not that it is declining. It is that it has been remaking itself — systematically, over decades — into a political economy that now reproduces the conditions preventing its own reform.

That distinction matters. Not just for Britain, but for every advanced anglosphere economy that followed a similar growth model and has not yet worked through its consequences.

Most commentary on Britain runs in two tracks. One blames immigration. The other blames austerity. Both are downstream of a growth model that increasingly relied on asset appreciation and financial expansion as productivity growth weakened — and that, in doing so, recomposed the electorate in its own image. The reforms that would reverse the model are now structurally resisted by the constituencies the model created. That is a different kind of problem than a bad policy cycle. It is a structural trap, and it is closing.

Britain is not alone in having built this model. It is simply the furthest along in working through its consequences. Australia and Canada, also anglosphere economies with financialised housing markets and political systems calibrated to the median property-owner, are approaching versions of the same juncture. Britain is the data point they should be reading carefully.

What 2012–2026 Actually Did

The post-2012 period is often read as a story of austerity, then Brexit, then stagnation. That reading misses the structural layer beneath it.

The underlying growth model shifted long before 2012. Since the 1980s, Britain progressively became more dependent on financial asset accumulation and housing appreciation as sources of wealth creation, while productivity growth weakened. By 2022, UK financial system assets stood at approximately £27 trillion — roughly 1,080% of GDP, up from 250% in 1980. By 2023, financial services contributed 8.8% of total UK economic output and generated a trade surplus of £73.2 billion, making Britain the world’s largest net exporter of financial services.

The problem is not the size of the financial sector. It is what grew in its shadow.

The significance of this shift was not simply that finance became larger. It was that an increasing share of national wealth became tied to the valuation of existing assets rather than the creation of new productive capacity. Rising asset values generated wealth, tax revenue, and political satisfaction even as underlying productivity performance weakened. The economy could continue producing gains for asset holders without generating equivalent gains in output per worker. Over time, this reduced the political urgency of addressing the productivity problem itself.

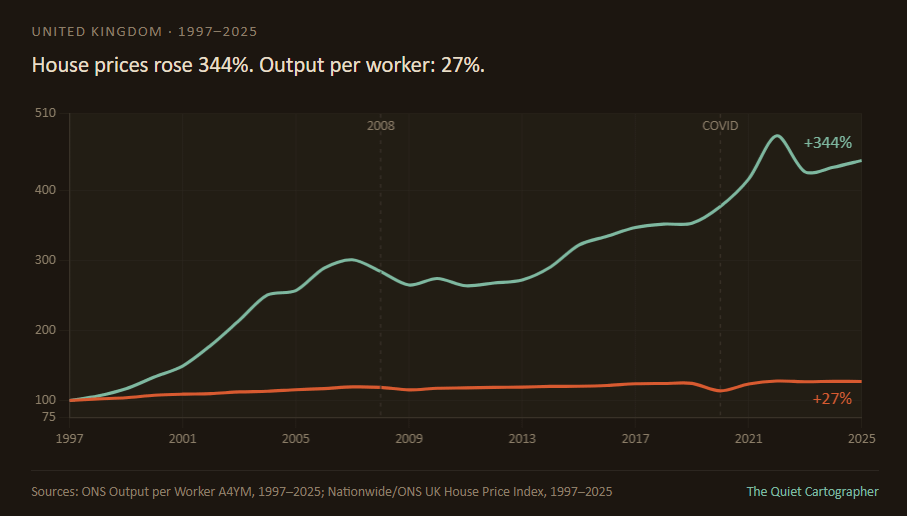

Productivity — the fundamental driver of sustainable wage growth — collapsed after 2008 and has not recovered. Between 1971 and 2007, output per employed person rose at 2.0% annually; between 2010 and 2024, it rose at just 0.2% per year. Multi-factor productivity in 2024 is estimated to have decreased compared to both 2023 and 2019, against a pre-2008 trend rate of roughly 1.8% annual growth. As a result, real wages did not return to their 2008 peak until 2024 — a sixteen-year stagnation without modern precedent. Had wages continued on their pre-crisis trajectory, the average worker would be earning approximately £11,000 more per year than they currently are.

As productivity-driven wage growth weakened, housing markets increasingly became the primary mechanism through which many households accumulated wealth. As wages stagnated, house prices continued rising — transferring wealth systematically from earners to owners. In 2008, climbing from the middle to the top of the wealth distribution required approximately ten years of full-time gross earnings; by 2018, it required almost sixteen. Those born in the 1980s are on track for lower homeownership rates than any cohort since the 1930s.

The 2012 period matters not because it initiated this dynamic, but because it locked it in. The post-2010 austerity settlement placed greater emphasis on fiscal restraint than on expanding productive investment. By the time Brexit arrived, the broad contours of the model had been evolving for more than thirty years. Brexit did not create the underlying weaknesses; it accelerated their exposure.

The important consequence was not merely economic. It was political. Asset inflation changed who owned wealth, who voted, and what voters sought to protect.

The Self-Sealing Mechanism

Here is the structural argument that conventional commentary tends to miss.

The constituencies that would bear the short-term costs of structural reform are the same constituencies that determine electoral outcomes.

The wealth gap between those in their early 60s and those in their early 30s reached approximately £150,000 in real terms by 2020–22, against near-nothing in 2006–08. The overall gap between the 5th and 9th wealth deciles now stands at £1.27 million — 37 times typical household income. This cohort not only holds the assets. It votes in disproportionate numbers, and its assets are directly sensitive to the reforms most likely to restore productive growth: planning liberalisation, property tax restructuring, pension fund redirection toward productive investment.

Every government that has attempted any of these has discovered the same ceiling. Post-2012 planning reform stalled. Help to Buy — designed as a demand stimulus — functioned in practice as a price support for the existing housing stock, widening the gap between those inside the market and those outside. Levelling Up was announced, underfunded, and quietly abandoned. The structural logic was the same in each case: the short-term losers were the electoral majority; the long-term beneficiaries were not yet in the market.

This is not a failure of political will. Treating it as such produces the wrong solutions — new leaders, new manifestos, new communication strategies. The mechanism is structural. The model increasingly aligned the interests of the electoral majority with the preservation of asset values, and the political system has responded accordingly.

Financial services became increasingly concentrated geographically, while much of the country’s productivity and investment challenge remained unresolved outside the South East. The ‘trickle-down from London finance’ argument has been extensively documented as exaggerated — and the regional inequality it was meant to offset has grown, not narrowed.

Why The Trap Tightens

Self-sealing systems become harder to change with time. As asset prices rise, more household wealth becomes dependent on their preservation. Retirement planning, local government revenues, bank balance sheets, and electoral incentives gradually adapt to the same underlying assumptions. Each adaptation creates an additional constituency with something to lose from disruption. The result is not a conspiracy against reform but an accumulation of veto points. By the time the costs of the model become widely recognised, a growing share of society has become invested in its continuation.

Why Conventional Solutions Fail

The standard reform agenda is real. Planning liberalisation. Infrastructure investment. Skills development. Industrial strategy. Long-horizon public investment. Each would, in principle, address some layer of the productivity problem over five to ten years.

The time-horizon problem is genuine: the political system rewards three-year results while structural reforms require decade-long payoffs. Most commentary stops there.

But the deeper problem is not the time horizon. It is who bears the costs in the short term and who captures the gains in the long term.

Planning reform reduces the asset value of existing homes and concentrates gains in future residents — a constituency that does not yet own and therefore votes less consistently for incumbents. Pension fund redirection toward productive investment reduces returns to current retirees and concentrates gains in future workers. Public investment financed through wealth or property taxes extracts from the asset-holding majority to fund services used disproportionately by the asset-poor.

The reform programme struggles to sustain itself because the constituencies that would benefit most from long-term restructuring remain politically weaker than those exposed to its short-term costs. Britain’s institutions remain functional, its research capacity world-class, its reform proposals technically sound. The constraint is not analytical. It is structural: the political economy has adapted around the model, and adaptation compounds.

What Economies Watching Should Read Into This

This matters beyond Britain.

Australia and Canada share enough of the structural architecture to read Britain as a forward projection rather than a cautionary tale from somewhere else. Both have financialised housing markets in which rising asset values have become an increasingly important source of household wealth as productivity-driven wage growth has slowed. Both have political systems calibrated to the interests of existing property owners. Both have metropolitan financial sectors that concentrate wealth geographically while claiming to generate diffuse national prosperity. Both are beginning to register the early symptoms.

The warning signs are identifiable before the trap closes. Productivity growth slows while housing wealth continues rising. Political debates become increasingly organised around protecting asset values rather than expanding productive capacity. Younger cohorts find themselves excluded from ownership while older cohorts grow increasingly dependent on asset appreciation for retirement security. Governments continue promising growth but rely increasingly on population expansion, property markets, and financial activity to generate it. Reform proposals repeatedly fail not because they lack technical merit but because they impose concentrated costs on politically powerful asset holders.

By the time these patterns become obvious, the political economy has already adapted around them. The constituencies that would lose from reform have become structurally entrenched. The constituencies that would gain are politically subordinate or not yet participating. The window for relatively low-cost structural adjustment has passed.

Self-sealing systems are difficult to reform, but not impossible; the point is that the political costs of reform rise as the system matures.

Britain reached that juncture sometime in the 2010s. It did not announce itself. It built, incrementally and through individually rational decisions, a political economy in which stagnation became the path of least resistance — and then discovered that the path was self-reinforcing.

The lesson is not that Britain's problems are unique. It is that the political conditions producing them are increasingly visible in other economies too.

Follow on X: The Quiet Cartographer

Really strong piece.

The £150,000 wealth gap between the early 60s and early 30s cohorts is concerning to say the least. That's not just inequality it's the political constituency that any reform programme has to defeat or wait out, and waiting out is the strategy that compounds the trap.

The thing I'd add, and I'm curious to get your thoughts on is how much of the trap is also generational lock-in through pension exposure?

A surprising share of asset-rich older households aren't just protecting their own house values - they're protecting the equity their workplace pensions are exposed to through commercial property, REITs, and the same domestic housing market. Which makes any reform that touches asset values feel like a double hit to them, even if they don't articulate it that way.

I'm curious, do you read the pension-housing entanglement as part of the self-sealing mechanism, or as a separate layer sitting on top of it?

Australia has much the same problems as the UK, but with the important advantage of a highly productive resources sector. The entitled classes respond with hysteria to any proposals which threaten their privileged position - e.g. the current squawking about changes to negative gearing and capital gains tax concessions. The Labor government's previous measures to limit the tax benefits of DIY superannuation funds provoked a similarly hysterical response. Unfortunately the current government has not yet managed to convince enough of the eventual beneficiaries - the young and poor - that these changes are in their interest.