From Tariffs to Tankers

Trade was the surface. The deeper contest is over the systems that make economies function — and the US Supreme Court just made that shift harder to ignore.

On February 20, 2026, the United States Supreme Court struck down the legal foundation of the president’s most-used economic instrument — and the administration replaced it before lunch.

The court ruled, 6–3, that the International Emergency Economic Powers Act does not authorise the president to impose tariffs. Within hours, Trump signed a proclamation imposing a 10% global tariff under Section 122 of the 1974 Trade Act. The next morning, he said it would rise to 15%. Treasury Secretary Bessent was explicit about the substitution: combining Section 122, Section 232, and Section 301 authorities, he said, would produce virtually unchanged tariff revenue.

The instrument changed. The pressure did not.

That is the useful fact.

Two months later, the scale of what had to be unwound became legible. On April 20, 2026, Customs and Border Protection launched a purpose-built portal to process refunds estimated at roughly $175 billion in IEEPA duties — a volume so large the agency calculated that manual processing would have required more than 4.4 million working hours. The court had removed the instrument. Now the state was being asked to refund what the instrument had already collected. The administrative machine required to undo a failed tariff is itself a demonstration of why the serious contest could not stay there.

The question the ruling asks

If the fastest executive lever for imposing economic pressure has been narrowed — and the replacements are slower, more procedural, and more easily litigated — where does the pressure go?

It does not disappear.

It migrates downward.

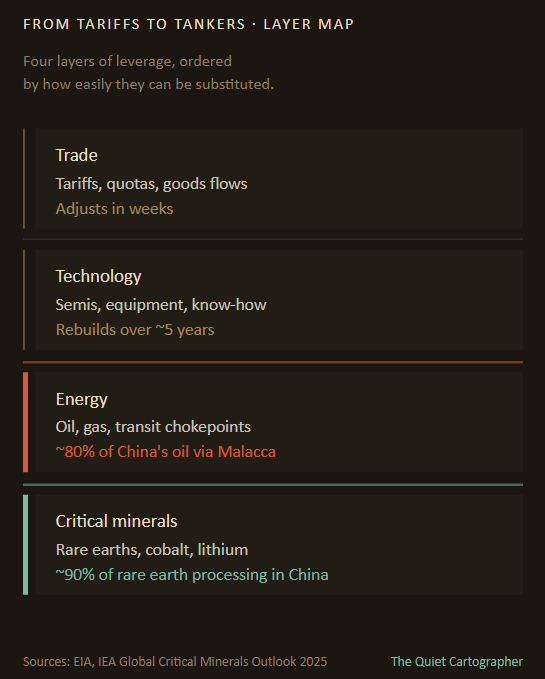

The layers

For most of the past decade, economic conflict appeared to centre on trade. Tariffs were the headline instrument, because they were visible, quantifiable, and politically legible. A 10% tariff could be announced on a Tuesday and appear in shipping invoices by Friday.

But trade was never the deepest layer of leverage. It was the most visible one.

Underneath it sit three others, each harder to substitute than the one above. And, each layer down is harder to reroute.

Layer one — trade

Trade is the most flexible layer. The first phase of US–China economic competition demonstrated this clearly. Tariffs reduced direct flows, but global supply chains adjusted. Production shifted to Vietnam, Mexico, and Malaysia. Costs rose, but the system kept working.

Trade friction is real. It is also adaptable.

That adaptability is precisely what limits its coercive power — and what made the February 20 ruling possible. Courts can strike down an instrument whose effects are visible, quantifiable, and attributable. A tariff has a statute, a rate, and a receipt.

The deeper layers do not.

Layer two — technology

The next phase moved into technology, most visibly in semiconductors.

Export controls on advanced chips and the equipment used to make them imposed constraints that do not reroute on weekly supply-chain timescales. They reshape capability over years. Unlike goods in a container, a fabrication plant cannot be rebuilt in a different country in a planning cycle.

Technology is less flexible than trade. Its rebuild clocks run in five-year increments, not quarterly ones. But technology is still substitutable — slowly, and at cost.

Layer three — energy

Energy occupies a different category altogether. It is not an input into production. It is a prerequisite for it.

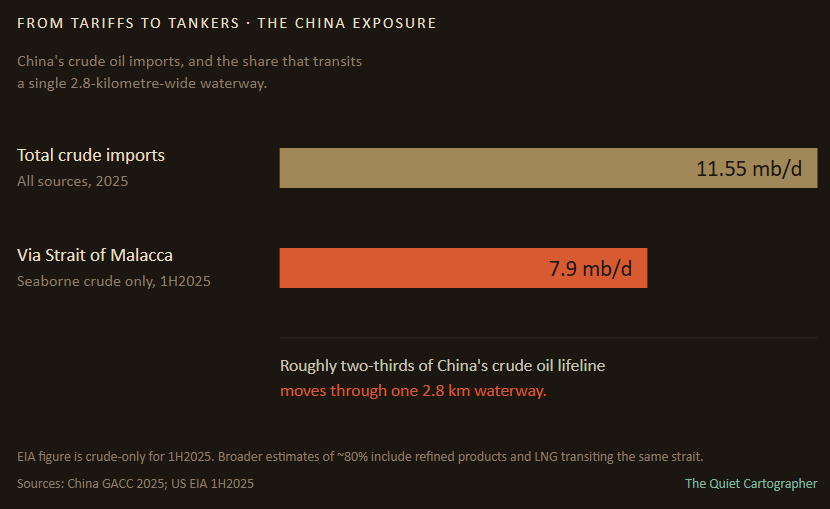

What makes energy distinct is that control does not require ownership. It can be shaped through access — through shipping routes, maritime insurance, financial clearing, and sanctions exposure. China imports a majority of its crude oil, and roughly 80% of those imports pass through a single waterway: the Strait of Malacca, 2.8 kilometres wide at its narrowest point.

China knows this. Beijing has spent two decades building overland pipelines from Russia, Kazakhstan, and Myanmar to reduce exposure. Those pipelines now carry roughly 3.7 million barrels per day. China’s 2025 crude imports averaged 11.55 million barrels per day — a record high — and its refiners processed over 14 million barrels per day.

The gap is not closing.

That dependency does not require a tariff to exercise. It requires a Lloyds of London insurance policy to lapse, a tanker’s flag to change, or a port to delay a clearance.

None of those instruments can be struck down by a court.

Layer four — critical minerals

Running alongside energy is a parallel system, gaining importance by the quarter: critical minerals.

Lithium, cobalt, rare earth elements. The inputs to batteries, magnets, electronics, and the defence supply chain.

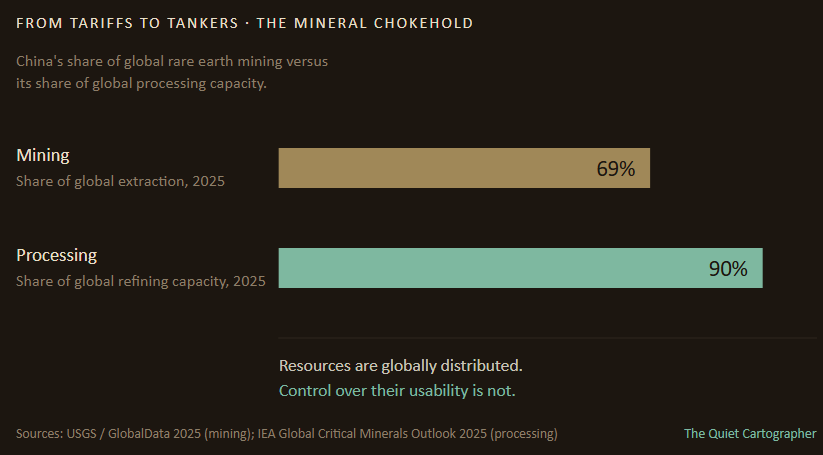

Here the control structure looks different from oil. Extraction is globally distributed — cobalt concentrates in the Democratic Republic of the Congo, lithium in the Lithium Triangle of Chile, Argentina, and Bolivia, rare earths in several countries including the United States itself. But processing — the step that turns ore into something usable — is concentrated overwhelmingly in China. The International Energy Agency puts China’s average share of processing for 19 of 20 strategic minerals at 70%. For rare earths specifically, China mines roughly 69% of global supply and processes closer to 90% of it.

The gap between those two numbers is the point. Resources are globally distributed. Control over their usability is not.

In October 2025, China formalised this leverage. Beijing announced new export controls requiring licences for rare earth mining and processing technologies, for magnet manufacturing, and — crucially — for any foreign firm wishing to supply rare earths that were extracted using Chinese technology, even if the extraction happened outside China.

The implication is straightforward: a country can lose its mining share to Australia or the US, but it does not lose its processing share until someone else builds the refineries — and refineries take the better part of a decade.

Control without ownership

That phrase is worth pausing on, because it describes the mechanism that connects all three lower layers.

The defining feature of competition at the energy and mineral layers is that it does not require ownership of the underlying resource. It requires control of one link in the chain that turns the resource into something usable.

Shipping routes. Maritime insurance markets. Financial clearing systems such as SWIFT. Processing licences. The list of chips in a stockpile. The list of vessels a reinsurer will cover.

None of these instruments appear in a tariff schedule. None can be invalidated by a 6–3 ruling on the statutory interpretation of a 1977 statute. They operate through private contracts, regulatory discretion, and commercial relationships — the layer underneath the layer that the law can reach quickly.

This is the shift that matters.

How pressure propagates — the fertilizer case

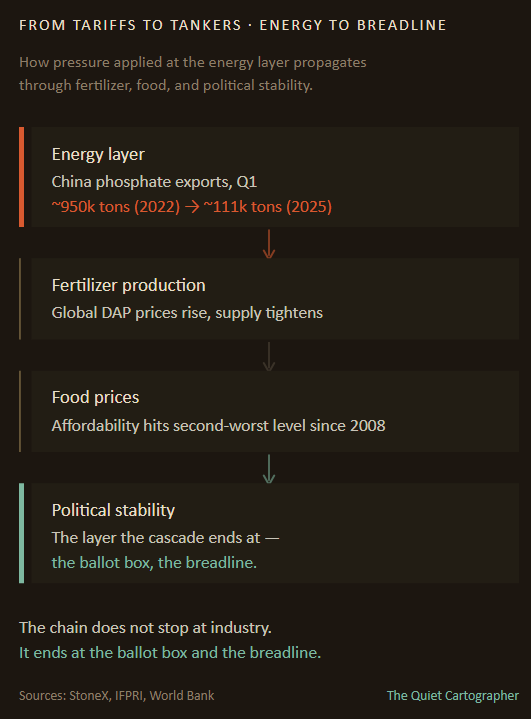

The clearest illustration that energy-layer leverage reaches beyond industry and into societies is the fertilizer market.

China accounts for roughly 30% of global phosphate fertilizer production. In December 2025, Chinese industry associations — coordinated under the direction of the National Development and Reform Commission — agreed to suspend new export orders for phosphate fertilizer until August 2026. The effect was already visible: in Q1 of 2022, a normal year, China exported roughly 950,000 tons of phosphate fertilizer; by Q1 of 2025, that figure had collapsed to around 111,000 tons — an ~88% decline. Chinese urea exports, historically 5–5.5 million tons per year, had similarly fallen to negligible levels.

Global prices moved in lockstep. DAP prices rose from $568 per metric ton in December 2024 to $615 by March 2025. By mid-2025, the fertilizer-to-corn affordability ratio in the United States was the second-worst since records began — beaten only by the 2008 spike.

The sequence that follows is mechanical:

Energy inputs (natural gas, sulphur) set the cost floor for fertilizer production.

Fertilizer availability sets the cost floor for agricultural output.

Agricultural output sets the cost floor for food prices.

Food prices set the floor for political stability.

The chain does not stop at industry. It ends at the ballot box and the breadline.

Europe as stress test

Europe has already run this experiment.

Following the disruption of Russian pipeline gas after 2022, Europe reconfigured its energy system at speed — shifting to liquefied natural gas imports and alternative suppliers under REPowerEU. Industrial electricity prices rose. Fertilizer production in several European regions contracted because it could not absorb the gas-price shock. Governments intervened to stabilise both energy and food markets.

The shock did not originate in trade. No tariff triggered it.

It originated in the energy layer and propagated outward — exactly as the model predicts.

Where competition moves

Return to the February 20 ruling, two months on. The road map is no longer speculative — it is visible in the Federal Register.

Section 122’s 10% tariff took effect February 24 and expires by statute on July 24, 2026. It is a bridge, not a destination, and it was always meant to be. On March 11, the US Trade Representative launched Section 301 investigations covering sixteen major trading partners on manufacturing overcapacity, and a separate investigation covering sixty countries on forced labour enforcement. On April 2, the administration imposed new Section 232 duties — up to 50% on steel, aluminium, and copper, up to 100% on pharmaceuticals and pharmaceutical ingredients. Section 122 expires in July. Section 232 tariffs have already been upheld by the Supreme Court. They do not expire.

The substitution is working exactly as Bessent described. The instruments are slower, more procedural, more investigation-driven — and more durable. Bessent’s commitment to virtually unchanged tariff revenue is on track to be met through a combination of statutes that were designed to survive court challenge in ways IEEPA was not.

Section 122 itself is already being contested. On March 5, twenty-four state attorneys-general filed suit in the Court of International Trade arguing that Section 122 was designed for balance-of-payments crises, not trade-deficit policy. The same court that struck down IEEPA is now being asked to strike down its bridge. If it does, the migration accelerates — not reverses. Section 232 and Section 301 become the only instruments left standing, and both were built for durability.

The cost of the instrument failing

The refund process itself demonstrates the article’s argument in a way the writing could not have scripted.

On April 20, 2026, Customs and Border Protection launched the CAPE portal — the Consolidated Administration and Processing of Entries — to handle what its own filings described as 4.4 million working hours of refund processing. Phase 1 covers roughly $127 billion of the estimated $175 billion owed. More than 56,000 importers had registered before launch. Refunds are projected within 60 to 90 days of approved declarations, disbursed electronically via ACH.

One category of claimant is excluded by design: consumers.

Businesses that paid IEEPA tariffs at the border get refunds. Households that paid higher shelf prices do not. The pressure flowed down the chain. The relief only flows up.

That is what it costs when an instrument fails in court. Not just the revenue — the state has to build new plumbing to unwind what the court undid, and the distributional asymmetry is locked in along the way. The instrument failed at the tariff layer. The relief fails at the consumer layer. And the next round of pressure has already moved on, to layers where this sequence does not repeat because no court can reach them.

The closing claim

Tariffs live in statute.

Control over the layers beneath them does not.

An insurance underwriter can decline to cover a vessel. A clearing bank can delay a payment. A processing licence can sit in a regulator’s inbox. A refinery can reject a cargo on technical grounds. None of these instruments require an executive order. None of them can be invalidated by a Supreme Court ruling, because none of them were legislated in the first place.

You cannot litigate an insurance certificate.

That is why, when one layer of competition is constrained by a court, the pressure does not disappear. It moves to a layer where the enforcement mechanism is not a statute, but a commercial decision — harder to see, harder to challenge, and much harder to strike down.

The ruling of February 20 did not end tariff competition. The portal that opened on April 20 did not end it either. Together, they demonstrated — cleanly and on the record — why the serious contest was never going to stay at the tariff layer for long.

Follow on X: The Quiet Cartographer

Sources and additional reading

Chinese phosphate exports plummet, dashing hope for price relief

Fact Sheet: President Donald J. Trump Imposes a Temporary Import Duty

International Emergency Economic Powers Act (IEEPA) Duty Refunds

Learning Resources, Inc., et al. v. Trump, President of the United States (2026)

Minerals with Net Import Reliance on China

Supreme Court Strikes Down IEEPA Tariffs: What Importers Need to Know Now

Trump administration launches tariff refund portal. Here’s what to know.

U.S. Energy Information Administration

With new export controls on critical minerals, supply concentration risks become reality